By Dan Kervick

One staple of economic policy debate is the running conflict between those who lean toward a reliance on fiscal policy and those who lean toward a reliance on monetary policy. Continue reading

By Dan Kervick

One staple of economic policy debate is the running conflict between those who lean toward a reliance on fiscal policy and those who lean toward a reliance on monetary policy. Continue reading

Posted in Dan Kervick, MMT, Modern Monetary Theory, Monetary policy

By Dan Kervick

The Unites States government operates a fiat currency system. The government is therefore the monopoly supplier of the final means of payment in our dollar-based economy, and is ultimately responsible, in one way or another, for any net increase in dollar-denominated financial assets in the private sector.

And yet, we continue to hear bipartisan expressions of fear and angst about the budget deficit and the national debt. Both major parties seemingly agree that we are “out of money”. They wrangle over various competing approaches to shrinking the gap between tax revenues and government spending. They appoint commissions to study the government budget and recommend some combination of slashed spending and higher taxes in order to close that budgetary gap. They warn us that we will transform ourselves into banana republic status if we do not urgently address our public debt problems.

This situation should be perplexing. Why does a government that is the issuer of the national currency have to borrow that currency back from the public to which the currency is issued? And how could such a government ever experience the kinds of budgetary squeezes and debt burdens that can pose severe problems for households and businesses?

I wish to make a radical suggestion: Public borrowing is an outdated practice, and we could dispense with it entirely. Borrowing by the public treasury and the accumulation of government debt obligations are legacies of the era that preceded the development of modern fiat currency, an era when governments were primarily users of traditional means of payment that lay outside their control, and not the producers and issuers of the primary means of payment. That pre-fiat era is now dead in the US, and the chief remaining role of government borrowing in our time is to bamboozle the public, and to obscure the true nature and effects of government fiscal and monetary operations under a bewildering maze of bookkeeping ink and financial legerdemain. Eliminating public borrowing, and replacing it with operations that are simpler, more direct and more transparent, would advance the cause of informed democratic debate over public spending and taxation. Above all, the change would eliminate needless obscurity and confusion and help us all understand exactly whose bread is being buttered by the budgetary decisions made by politicians.

Posted in Michael Hudson, Monetary policy, Regulation, Uncategorized

Tagged deregulation, Michael Hudson, Monetary policy, regulation

The following is a paper given at the ASSA conference in Denver this past week for a panel organized by James Galbraith, titled Pressures on the Paradigm, sponsored by Economists for Peace & Security.

The Queen famously asked her economists why none had seen the global crisis coming. Obviously the answer is complex, but it must include the evolution of economic theory over the postwar period—from the “Age of Keynes”, through the Friedmanian era and the return of virulent Neoclassical economics, and finally on to the New Monetary Consensus with a New anti-Keynesian version of fine-tuning by an unaccountable (“independent”) central bank

We cannot leave out the parallel developments in finance theory—with its efficient markets hypothesis—and the subsequent deregulation and de-supervision that led to the financialization of everything.

But to make a long story short: if your theory says that a global collapse is impossible, you won’t see one coming. In truth, as Jamie has argued in his great book, the Predator State, no one outside Chicago and other institutes of the higher learning ever took the free market mantra seriously—outside the ivory towers it was nothing but a slogan, a justification for enrichment of the powerful few.

Like Jamie, I believe orthodox macroeconomics is finished—although not all the zombie practitioners of that dismal religion recognize they are dead. After the crisis hit, Jamie, Duncan Foley and I were invited to appear on panels at the University of Chicago along with a dozen or so of the Chicago boys.

Not surprisingly, none of them was budging from his dogma of free and efficient markets: the crisis was caused by too much government interference; the solution is more deregulation. Three years into this crisis those who never saw it coming proclaim signs of recovery everywhere they look.

And, still, it is only academia that is clueless. Everyone in financial markets saw it coming—indeed, they planned on it and worked fastidiously to create it. They would profit on the way up, and then profit more in the collapse whilst collecting on their credit default swap bets and stealing all the homes.

It is Bush’s ownership society and the goal all along was to transfer all ownership to the top through the creation of serial bubbles—what Michael Hudson calls Bubbleonia. The biggest land grab since the enclosure movement.

So, no, there is no recovery. The banks are more massively insolvent than they were 2 years ago. They are cooking their books so they can pay executive bonuses and reward the traders and the foreclosers who are successfully transferring all wealth to the elite.

But Jamie asked me to address the state of theory—not the economy.

I want to focus on one particular Zombie that needs a stake through its heart or a bullet through its head: the New Monetary Consensus. This is an updated New Keynesian version of the old Bastard ISLM model.

The idea is that inflation slows growth so it must be diligently fought. The Fed will keep inflation expectations low, inflation will be low, and growth will be robust.

Every link in that sentence is a delicious illusion.

The Fed supposedly manages expectations by convincing markets that it controls inflation, and so long as it controls expectations it can control inflation.

But if it cannot control expectations it cannot manage inflation and all bets are off. What a flimsy reed upon which to hang public policy!

And in any case, why should low inflation generate robust growth? Because—well, because the Fed says it will, contrary to all evidence.

Out in the real world, expectations alone cannot govern any economic phenomena: inflation expectations will determine actual inflation only if those with ability to influence prices act on those expectations. And inflation below the high double digits has never proven to be a barrier to economic growth.

Let us take the current experience as an example. We have moved on to QE2, an application of the NMC.

Helicopter Ben is supposedly injecting trillions of dollars of money into the economy to create expectations of inflation—to counter the deflationary real world forces. And many wingnuts actually ARE expecting inflation—running around like Chicken-Littles, buying gold and screaming about hyperinflation and collapse of the dollar. And, yet, no inflation. Why?

Because those who might have pricing power—corporations and organized labor—cannot create inflation. Workers cannot increase their wages given massive global unemployment, and firms cannot increase prices in the face of competitive pressures. So no matter how strong is the will to believe, it has no purchase against the facts.

The wingnuts will be proven wrong. The Fed cannot create inflation. It is within the power of the central bank to lower the price of reserves—the overnight rate–as close to zero as it wants. It can also lower longer term rates on assets it is willing to buy, but there is a nonzero practical limit to that based on what Keynes called the square rule.

Quantitative easing supposedly pumps money into the economy to generate spending in order to create expectations of inflation. But all it really amounts to is substituting reserves for treasuries on bank balance sheets—lowering their interest earnings. QE won’t work because:

• (1) additional bank reserves do not enable or encourage greater bank lending;

• (2) the interest rate effects are small at best, and are swamped by private sector attempts to deleverage;

– The best estimate based on NYFed work: 18 basis points

• (3) purchases of Treasuries are simply an asset swap that reduce the maturity of private sector assets, but do not raise private sector incomes; and

• (4) given the reduced maturity of private sector portfolios, reduced interest income could actually be deflationary.

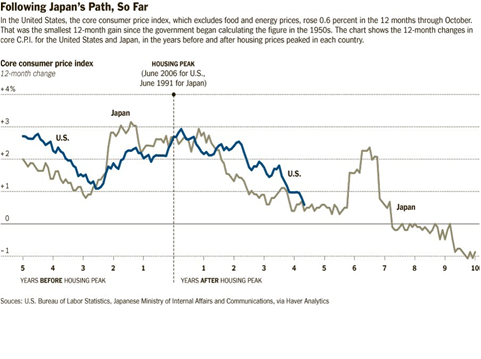

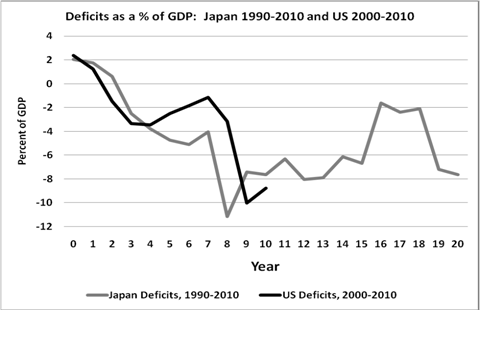

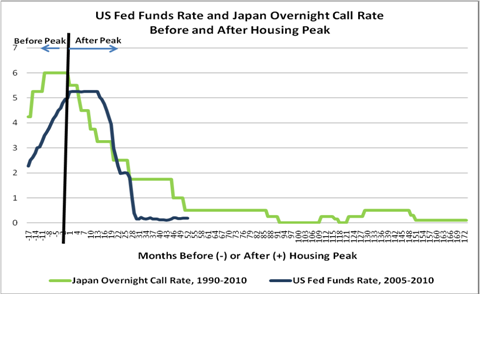

But we knew all that—Japan has been doing QE for 20 years, trying to create expectations of inflation in the face of deflationary headwinds, thus, it is interesting to compare Japanese and US experience (so far) by looking at a series of three graphs.

As they say, history doesn’t repeat itself but in this case it rhymes nicely. Only insanity would lead us to follow Japan’s path while expecting different results.

Let me finish my critique of the NMC with an observation of a Galbraith—John Kenneth this time:

To limit unemployment and recession in the US and the risk of inflation, the remedial entity is the Fed… For many years (with more to come) this has been under the direction from Washington of a greatly respected chairman… The institution and its leader are the ordained answer to both boom and inflation and recession or depression… Quiet measures enforced by the Fed are thought to be the best approved, best accepted of economic actions. They are also manifestly ineffective. They do not accomplish what they are presumed to accomplish. Recession and unemployment or boom and inflation continue. Here is our most cherished and, on examination, most evident form of fraud.

Even if the early postwar “Keynesian” economics had little to do with Keynes at least it had some connection to the real world. What passed for macroeconomics on the precipice of the global collapse had nothing to do with reality—it is as relevant to our economy as flat earth theory is to natural science.

In short, expecting the Queen’s economists to foresee the crisis would be like putting flat- earthers in charge of navigation for NASA and expecting them to accurately predict points of re-entry and landing of the space shuttle. Of course, the economic advisors to Presidents Bush and Obama could do no better.

Referring to the work of the best known economists over the past thirty years, Lord Robert Skidelsky argues “Rarely in history can such powerful minds have devoted themselves to such strange ideas.” Not only were they strange, but the ideas of the Larry Summers’, Bob Rubins, Mankiws, Marty Feldsteins, Bernankes and John Taylors of the world were, predictably, dangerous.

But one economist got it right, and did see it coming. And that is Hyman Minsky. His theory said it can happen again: market forces are destabilizing.

The economy emerged from WWII with a robust financial system—hardly any private debt and lots of safe and liquid government debt. Various New Deal and postwar reforms also made the economy stable: a safety net that stabilized consumption; strict financial regulation; minimum wage laws and support of unions; low cost mortgages and student loans, and so on. And memories of the Great Depression discouraged risky behavior.

Gradually all that changed—memories faded, self-regulation replaced financial regulations, unions lost power and government support, globalization brought low-wage competition, and the safety net was shredded. Further, profit-seeking firms and financial institutions took on greater risks with ever more precarious finance. Thus, fragility grew on trend. This made “it” possible again.

While most who invoke Minsky focus on the crash, he believed that the main instability is a tendency toward explosive euphoria. High aggregate demand and profits associated with high employment raise expectations and encourage increasingly risky ventures based on commitments of future revenues that will not be realized.

A snowball of defaults then leads to a debt deflation and high unemployment unless there are “circuit breakers” that intervene to stop the market forces. The main circuit breakers, are the Big Bank (central bank as lender of last resort) and Big Government (countercyclical budget deficits).

And, boy-oh-boy have we got a Big Bank and a Big Government! Together, the Benny and Timmy tag team have spent, lent, or guaranteed $25 trillion in the name of Uncle Sam. And that still is not enough. “It” is still happening.

The problem is that most of this was done by the Big Bank Fed, aimed at helping financial institutions—trying to prop up their worthless assets. In short, it was based on the theory that we need Money Manager capitalism and that the only hope is to generate another bubble.

It won’t work. Financialization is the problem, not a sustainable economic strategy. We need to turn instead to an updated Keynesian-Minskian New Deal based on jobs, growing wages, consumption—especially public consumption, constrained and downsized finance, and greater equality. Monetary policy also has to be downsized, while fiscal policy has to play a bigger role. Not fine-tuning but a positive and permanent presence to counter and guide and supplement the private purpose.

More importantly we’ve got to formulate theory applicable to the world in which we actually live—not one in which imaginary representative agents allocate resources along an optimal consumption path.

To that end, we stand on the shoulders of the giants like Minsky in the heterodox tradition.

Posted in Monetary policy, Uncategorized

Proposals for the Banking System

The hard lesson of banking history is that the liability side of banking is not the place for market discipline. Therefore, with banks funded without limit by government insured deposits and loans from the central bank, discipline is entirely on the asset side. This includes being limited to assets deemed ‘legal’ by the regulators and minimum capital requirements also set by the regulators.

Given that the public purpose of banking is to provide for a payments system and to fund loans based on credit analysis, additional proposals and restrictions are in order:

1. Banks should only be allowed to lend directly to borrowers, and then service and keep those loans on their own balance sheets. There is no further public purpose served by selling loans or other financial assets to third parties, but there are substantial real costs to government regarding the regulation and supervision of those activities. And there are severe consequences for failure to adequately regulate and supervise those secondary market activities as well. For that reason (no public purpose and geometrically growing regulatory

burdens with severe social costs in the case of regulatory and supervisory lapses), banks should be prohibited from engaging in any secondary market activity. The argument that these areas might be profitable for the banks is not a reason to extend government sponsored enterprises into those areas.

2. US banks should not be allowed to contract in LIBOR. LIBOR is an interest rate set in a foreign country (the UK) with a large, subjective component that is out of the hands of the US government. Part of the current crisis was the Federal Reserve’s inability to bring down the LIBOR settings to its target interest rate, as it tried to assist millions of US homeowners and other borrowers who had contacted with US banks to pay interest based on LIBOR settings. Desperate to bring $US interest rates down for domestic borrowers, the Federal Reserve resorted to a very high risk policy of advancing unlimited, functionally unsecured, $US lines of credit called ‘swap lines’ to several foreign central banks. These loans were advanced at the Fed’s low target rate, with the hope that the foreign central banks would lend these funds to their member banks at the low rates, and thereby bring down the LIBOR settings and the cost of borrowing $US for US households and businesses. The loans to the foreign central banks peaked at about $600 billion and did eventually work to bring down the LIBOR settings. But the risks were substantial. There is no way for the Fed to collect a loan from a foreign central bank that elects not to pay it back. If, instead of contracting based on LIBOR settings, US banks had been linking their loan rates and lines of credit to the US fed funds rate, this problem

would have been avoided. The rates paid by US borrowers, including homeowners and businesses, would have come down as the Fed intended when it cut the fed funds rate.

3. Banks should not be allowed to have subsidiaries of any kind. No public purpose is served by allowing bank to hold any assets ‘off balance sheet.’

4. Banks should not be allowed to accept financial assets as collateral for loans. No public purpose is served by financial leverage.

5. US Banks should not be allowed to lend off shore. No public purpose is served by allowing US banks to lend for foreign purposes.

6. Banks should not be allowed to buy (or sell) credit default insurance. The public purpose of banking as a public/private partnership is to allow the private sector to price risk, rather than have the public sector pricing risk through publicly owned banks. If a bank instead relies on credit default insurance it is transferring that pricing of risk to a third party, which is counter to the public purpose of the current public/private banking system.

7. Banks should not be allowed to engage in proprietary trading or any profit making ventures beyond basic lending. If the public sector wants to venture out of banking for some presumed public purpose it can be done through other outlets.

8. My last proposal for the banks in this draft is to utilize FDIC approved credit models for evaluation of bank assets. I would not allow mark to market of bank assets. In fact, if there is a valid argument to marking a particular bank asset to market prices, that likely means that asset should not be a permissible bank asset in the first place. The public purpose of banking is to facilitate loans based on credit analysis rather, than market valuation. And the accompanying provision of government insured funding allows those loans to be held to maturity without liquidity issues, in support of that same public purpose. Therefore, marking to market rather

than evaluation by credit analysis both serves no further public purpose and subverts the existing public purpose of providing a stable platform for lending.

Proposals for the FDIC (Federal Deposit Insurance Corporation)

I have three proposals for the FDIC. The first is to remove the $250,000 cap on deposit insurance. The public purpose behind the cap is to help small banks attract deposits, under the theory that if there were no cap large depositors would gravitate towards the larger banks. However, once the Fed is directed to trade in the fed funds markets with all member banks, in unlimited size, the issue of available funding is moot.

The second is to not tax banks in order to recover funds lost on bank failures. The FDIC should be entirely funded by the US Treasury. Taxes on solvent banks should not be on the basis of the funding needs of the FDIC. Taxes on banks have ramifications that can either serve or conflict with the larger public purposes presumably served by government participation in the banking system. These include sustaining the payments system and lending based on credit analysis. Any tax on banks should be judged entirely by how that tax

serves or doesn’t serve public purpose.

My third proposal for the FDIC is to do its job without any assistance by Treasury (apart from funding any FDIC expenditures). The FDIC is charged with taking over any bank it deems insolvent, and then either selling that bank, selling the bank’s assets, reorganizing the bank, or any other similar action that serves the public purpose government participation in the banking system. The TARP program was at least partially established to allow the US Treasury to buy equity in specific banks to keep them from being declared insolvent by the FDIC, and to allow them to continue to have sufficient capital to continue to lend. What the

TARP did, however, was reveal the total failure of both the Bush and Obama administrations to comprehend the essence of the workings of the banking system. Once a bank incurs losses in excess of its private capital, further losses are covered by the FDIC, an arm of the US government. If the Treasury ‘injects capital’ into a bank, all that happens is that once losses exceed the same amount of private capital, the US Treasury, also an arm of the US government is next in line for any losses to the extent of its capital contribution, with the FDIC covering any losses beyond that. So what is changed by Treasury purchases of bank equity? After the private capital is lost, the losses are taken by the US Treasury instead of the FDIC, which also gets its funding from the US Treasury. It makes no difference for the US government and the ‘taxpayers’ whether the Treasury covers the loss indirectly when funding the FDIC, or directly after ‘injecting capital’ into a bank. All that was needed to accomplish the same end as the TARP program- to allow banks to continue to function and acquire FDIC insured deposits- was for the FDIC to directly reduce the private capital requirements. Instead, and as direct evidence of a costly ignorance of the dynamics of the banking model, both the Obama and Bush administrations burned through substantial quantities of political capital to get the legislative authority to allow the Treasury to buy equity positions in dozens of private banks. And, to make matters worse, it was all accounted for as additional federal deficit spending. While this would not matter if Congress and the administrations understood the monetary system, the fact is they don’t, and so the TARP has therefore restricted their inclination to make further fiscal adjustments to restore employment and output. Ironically, the overly tight fiscal policy continues to contribute to the rising delinquency and default rate for

bank loans, which continues to impede the desired growth of bank capital.

Proposals for the Federal Reserve

Proposals for the Treasury

Conclusion

I conclude with my proposals to support aggregate demand and restore output and employment.

Warren Mosler

October 11, 2009

President, Valance Co.

www.moslereconomics.com

www.mosler2012.com

Here’s the problem with that policy. Rising prices for housing have increased the cost of living and doing business, widening the excess of market price over socially necessary costs. In times past the government would have collected the rising location rent created by increasing prosperity and public investment in transportation and other infrastructure making specific sites more valuable. But in recent years taxes have been rolled back. Land sites still cost as much as ever, because their price is set by the market. Land itself has no cost of production. Locational value is created by society, and should be the natural tax base because a land tax does not increase the price of real estate; it lowers it by leaving less “free” rent to be paid to the banks.

The problem is that what the tax collector relinquishes is now available to be paid to banks as interest. And prospective buyers bid against each other until the winner is whoever is first to pay the land’s location rent to the banks as interest.

This tax shift – to the benefit of the bankers, not homeowners – has made Mr. Obama’s hope of doubling U.S. exports during the next five years ring hollow. This is the upshot of “creating wealth” in the form of a debt-leveraged real estate and stock market bubble. Labor must pay more for debt-financed housing and education, not to mention payments to health insurance oligopoly and higher sales and income taxes shifted off the shoulders of financial and real estate.

Once the Republicans were certain which way the vote would go, they were able to voice some nice populist sound bites for the mid-term elections this November. Jeff Sessions of Alabama and Sam Brownback of Kansas voted against Mr. Bernanke’s confirmation. Jim deMint of South Carolina warned that reappointing him would be “The biggest mistake that we’re going to make for a long time.” He added: “Confirming Bernanke is a continuation of the policies that brought our economy down.”

Among Democrats running for re-election, Barbara Boxer of California pointed out that by spurring the asset-price inflation, the Fed’s pro-Bubble (that is, pro-debt policy) has crashed the economy, shrinking employment. The Fed is supposed to protect consumers, yet Mr. Bernanke is a vocal opponent of the Consumer Finance Products Agency, claiming that the deregulatory Fed alone should be the sole financial regulator – seemingly an oxymoron.

Mr. Obama supports Mr. Bernanke and his State of the Union address conspicuously avoided endorsing the Consumer Financial Products Agency that he earlier had claimed would be the centrepiece of financial reform. Wall Street lobbyists have turned him around. Their logic was the same mantra that Connecticut insurance industry’s Sen. Chris Dodd repeated at the confirmation hearings: Mr. Bernanke has “saved the economy.”

How can the Fed be said to do this when the volume of debt is growing exponentially beyond the ability to pay? “Saving the debt” by bailing out creditors – by adding bad private-sector debts to the public sector’s balance sheet – is burdening the economy, not saving it. The policy only postpones the crisis while making the ultimate volume of debt that must be written off higher – and therefore more traumatic to write off, annulling a corresponding volume of savings on the other side of the balance sheet (because one party’s savings are another’s debts).

What really is at issue is the economic philosophy that Mr. Bernanke will apply during the coming four years. Unfortunately, Mr. Bernanke’s questioners failed to ask relevant questions along these policy lines and the economic theory or rationale underlying his basic approach. What needed to be addressed was not just his deregulatory stance in the face of the Bubble Economy and exploding consumer fraud, or even the mistakes he has made. Republican Sen. Jim Bunning elicited only smirks and pained looked as Mr. Bernanke rested his chin on his hand, as if to say, “I’m going to be patient and let you rant.” The other Senators were almost apologetic.

One popular (and thoroughly misleading) description of Bernanke that has been cited ad nauseum to promote his reappointment is that he is an expert on the causes of the Great Depression. If you are going to create a new crash, it certainly helps to understand the last one. But economic historians who have compared Mr. Bernanke’s writings to actual history have found that it is precisely his misunderstanding of the Depression that is leading him tragically to repeat it.

As a trickle-down apologist for high finance, Prof. Bernanke has drawn systematically wrong conclusions as to the causes of the Great Depression. The ideological prejudice behind his view is of course what got him his job in the first place, for as numerous observers have quipped, a precondition for being hired as Fed Chairman is that one does not understand how the financial system actually works. Instead of recognizing that deepening debt, low wages and the siphoning up of wealth to the top of the economic pyramid were primary causes of the Depression, Prof. Bernanke attributes the main problem simply to a lack of liquidity, causing low prices.

As my Australian colleague Steve Keen recently has written in his Debtwatch No. 42, the case against Mr. Bernanke should focus on his neoclassical approach that misses the fact that money is debt. He sees the financial problem as being too low a price level for assets to be collateralized for bank loans. And to Mr. Bernanke, “wealth” is synonymous with what banks will lend, under existing credit terms.

In 1933, the economist Irving Fischer (mainly responsible for the “modern” monetarist tautology MV = PT) wrote a classic article, “The Debt-Deflation Theory of the Great Depression,” recanting the neoclassical view that had led him to lose his personal fortune in the 1929 stock market crash. He explained how the inability to pay debts was forcing bankruptcies, wiping out bank credit and spending power, shrinking markets and hence the incentive to invest and employ labor.

Mr. Bernanke rejects this idea, or at least the travesty he paraphrases in his Essays on the Great Depression (Princeton, 2000, p. 24), as Prof. Keen quotes:

Fisher’ s idea was less influential in academic circles, though, because of the counterargument that debt-deflation represented no more than a redistribution from one group (debtors) to another (creditors). Absent implausibly large differences in marginal spending propensities among the groups, it was suggested, pure redistributions should have no significant macroeconomic effects.

The reality is that wealthy Wall Street financiers who make multi-million dollar salaries and bonuses spend their money on trophies: fine arts, luxury apartments or houses in gated communities, yachts, fancy handbags and high fashion, birthday parties with appearances by modish pop singers. (“I see the yachts of the stock brokers; but where are those of their clients?”) This is not the kind of spending that reflects the “real” economy’s production profile.

Mr. Bernanke sees no problem, unless rich people spend less of their gains on consumer goods and the products of labor than average wage earners. But of course this propensity to consume is precisely the point John Maynard Keynes made in his General Theory (1936). The wealthier people become, the lower a proportion of their income they consume – and the more they save.

This falling propensity to consume is what worried Keynes about the future. He imagined that as economies saved more as their income levels rose, they would spend less on goods and services. So output and employment would not be able to keep pace – unless the government stepped in to make up the gap.

Consumer spending is indeed falling, but not because economies are experiencing a higher net saving rate. The U.S. saving rate has fallen to zero – because despite the fact that gross savings remain high (about 18 percent), most is lent out to become other peoples’ debts. The effect is thus a wash on an economy-wide basis. (18 percent saving less 18 percent debt = zero net saving.)

The problem is that workers and consumers have gone deeper and deeper into debt, saving less and less. This is just the opposite of what Keynes forecast. Only the wealthiest 10 percent or so of the population save more and more – mainly in the form of loans to the “bottom 90 percent.” Saving less, however, goes hand in hand with consuming less, because of the revenue that the financial sector drains out of the “real” economy’s circular flow (wage-earners spending their income to buy the goods they produce) as debt service. The financial sector is wrapped around the production-and-consumption economy. So an inability to consume is part and parcel of the debt problem. The basis of monetary policy throughout the world today therefore should be how to save economies from shrinking as a result of their exponentially growing debt overhead.

Bernanke’s apologetics for finance capital: Economies seem to need more debt, not less

Bernanke finds “declines in aggregate demand” to be the dominant factor in the Great Depression (p. ix, as cited by Steve Keen). This is true in any economic downturn. In his reading, however, debt seems not to have anything to do with falling spending on what labor produces. Taking a banker’s-eye view, he finds the most serious problem to be the demand for stocks and real estate. Mr. Bernanke promises not to let falling asset demand (and hence, falling asset prices) happen again. His antidote is to flood the economy with credit as he is now doing, emulating Alan Greenspan’s Bubble policy.

The wealthiest 10 percent of the population do indeed save most of their money. They lend savings – and create new credit – to the bottom 90 percent, or gamble in derivatives or other zero-sum activities in which their gain (if indeed they make any) finds its counterpart in some other parties’ loss. The system is kept going not by government spending, Keynesian-style, but by new credit creation. That supports consumption, and indeed, lending against real estate, stocks and bonds enables borrowers to bid up their prices, enabling their owners to borrow yet more against these assets. The economy expands – until current revenue no longer covers the debt’s carrying charges.

That’s what brings the Bubble Economy down with a crash. Asset-price inflation gives way to crashing prices and negative equity for real estate and for much financial debt leveraging as well. It is in this sense that Prof. Bernanke’s blames the Depression on lower prices. When prices for real estate or other collateral plunge, it no longer can be pledged for more loans to keep the circular flow of lending and debt repayment in motion.

This circular financial flow is quite different from the circular flow that Keynes (and Say’s Law) discussed – the circulation where workers and their employers spent their wages and profits on consumer goods and investment goods. The financial circular flow is between the banks and their clients. And this circular flow swells as it diverts more and more spending from the “real” economy’s circular flow between income and spending. Finance capital expands relative to industrial capital*.

Higher prices in the “real” economy may help maintain the circular financial flow, by giving borrowers more current income to pay their mortgages, student loans and other debts. Mr. Bernanke accordingly sees FDR’s devaluation of the dollar as helping reflate prices.

Today, however, a declining dollar would make imports (including raw materials as well as key consumer goods) more costly. This would squeeze the budgets of most families, given America’s rising import dependency as its economy is post-industrialized and financialized. So Mr. Bernanke’s favored policy is to get banks lending again – not for the government to spend more on deficit spending on infrastructure, social services or other full employment projects. The government spending that Mr. Bernanke has endorsed is pure bailouts to the banks, insurance companies, real estate packagers and other Wall Street institutions so that they can support asset prices and thereby save the economy’s financial balance sheet, not its employment and living standards.

We’re getting closer to the point discussed a few weeks ago about markets giving up on the Fed.

Now that the bets have been placed, and none of that is happening, it’s all starting to erode. Crude is back below 75 (the Saudis’ actual target/range?), gold is selling off, the dollar is edging higher, the 10 year just traded at 3.57, stocks are selling off, etc.

Should market psychology turn to the notion that the Fed has no tools to inflate, and we have a Congress dead set against larger deficits, it can all get very ugly very quickly in the race to the exit from the inflation plays (including steepeners) currently on the books.

1. He does not understand that “unwinding” the Fed’s balance sheet is nothing to be concerned about. As I have written previously, this will occur naturally as banks pay-off their loans that the Fed extended in the crisis, and as banks repurchase the assets they sold to the Fed to obtain reserves. However, Bernanke still seems to believe in the discredited “deposit multiplier” and believes the Fed will have to take action to drain reserves (“reverse the quantitative easing”) to prevent excess reserves from fueling inflation. This is nonsense. Banks do not lend reserves and existence of excess reserves does not make them more willing to lend. The Fed does not need to do anything more than to accommodate banks—no concerted action is required. Still, even in the worst case, the Fed will not be able to create a huge mess. Since it operates with an overnight interest rate target, if it tries to remove reserves that the banks want to hold, it will drive rates above the target—so will have to add back the reserves. This could create some uncertainty but it is not likely to generate any crisis.

2. Bernanke might appear to be a “born again” regulator, but that is highly doubtful. The Fed will never take regulation seriously because it is captured by Wall Street. So the important thing is to ensure that the Fed does not become the “super duper systemic regulator” that many are now proposing. This job needs to go to the FDIC, which has in the past actually done some regulating.

3. A win for Bernanke might energize the forces that want to keep Timmy Geithner and Larry Summers in their jobs. In truth, it is far more important to remove Timmy and Larry (and to remove Robert Rubin from his position as advisor to the administration). I have not seen any evidence that Bernanke has been corrupted by Wall Street. Unfortunately, the same cannot be said of Geithner and Summers—where apparent conflicts of interest abound, and questionable decisions have been taken that favor Wall Street institutions. And the Treasury is far more important than the Fed. If we are going to reregulate financial institutions (as Obama now seems inclined to do), we have got to have real regulators at the Treasury. Neither Timmy nor Larry has ever indicated any interest in “interfering” with Wall Street. Indeed, Geithner seems to have been leaking to the press his dissatisfaction with Obama’s recent proposals. Perhaps he is already angling for his Wall Street rewards—seeking a well-compensated position in a financial institution should he be fired.

To be clear, I would prefer to replace Bernanke with someone who actually understands monetary policy and who advocates regulation and supervision of financial institutions. Unfortunately, that looks unlikely. We need to turn our attention to Rubin, Geithner and Summers. Obama does not need any action by Congress to rid himself of these anchors that are dragging down his administration, as well as the Democratic party.

Posted in L. Randall Wray, Monetary policy, Uncategorized

Tagged L. Randall Wray, Monetary policy

BERNANKE’S APOLOGY FALLS FLAT

By L. Randall Wray

There appear to be at least three reasons for Bernanke’s admission that the Fed did not do its job. First, and most obviously, Bernanke is up for reappointment (his term expires January 31)—and he will not sail through. The public is mad as hell, and politicians will have to put him through the wringer or face voter’s wrath in the next election. So Bernanke will have to appear contrite, and will apologize for his misdeeds many more times while Congress makes him sweat it out.

Second, Congress is actually considering whether it should strip the Fed of all regulatory and supervisory authority, given its miserable performance over the past decade—during which the Fed has consistently demonstrated that it has neither the competence nor the will to restrain Wall Street’s bankers. Since Greenspan took over the helm, the Fed has never seen a financial instrument or practice that it did not like—no matter how predatory or dangerous it was. Adjustable rate mortgages with teaser rates that would reset to levels guaranteed to produce defaults? Greenspan praised them (see here). Liar loans? Bring them on! NINJA loans (no income, no job, no assets)? No problem! Credit default swaps that let one gamble on the death of assets, firms, and countries? Prohibit government from regulating them! So Bernanke has to grovel and beg Congress to let the Fed retain at least some of its authority.

Third, many commentators blame the Fed for the crisis, arguing that it kept interest rates too low for too long, fueling the real estate bubble. Bernanke argues “When historical relationships are taken into account, it is difficult to ascribe the house price bubble either to monetary policy or to the broader macroeconomic environment”. If he can convince Congress that the problem was lack of oversight and regulation he can shift at least some of the blame to Treasury and Congress—since it was Treasury Secretary Rubin, and his protégé Summers, as well as Barney Frank, Christopher Dodd, and many others (significantly, Democrats who will now decide the Fed’s fate) who pushed through the deregulation bills in 1999 and 2000. He figures that if the Fed now supports re-regulation, he will be forgiven and the Democrats will be too embarrassed to admit their own misdeeds. (Significantly, Dodd has announced his retirement, in recognition of the role he played in creating the crisis. Another mea culpa on the way?)

While I do believe the Fed should be stripped of all such authority, I am sympathetic to his argument about monetary policy. Low interest rates do not cause bubbles. The Fed kept interest rates low after the NASDAQ crash because it feared deflation in the face of significant downward pressures on wages and prices globally (see here). The belief was that low interest rates would keep borrowing costs low for firms and households, helping to promote spending and recovery. In truth, spending is not very interest sensitive and the economy stumbled along in a “jobless recovery” in spite of the low rates. What was actually needed was a fiscal stimulus (if anything, low rates are counterproductive because they reduce government interest spending on its debt—as Japan’s experience taught us over the past couple of decades—but that is a point for another blog).

Still, the Fed was following conventional wisdom, and only began to gradually raise rates when job growth picked up in 2004. Over the following years, the Fed kept raising rates, and economic growth improved. (So much for conventional wisdom!) The worst excesses in real estate markets began only after the Fed had started raising rates, and lending standards continued their downward spiral the higher the Fed pushed its target interest rate. In other words, contrary to what many are arguing, the Fed DID raise rates but this had no impact in real estate markets.

Why not? Two main reasons. First, recall that Greenspan had promoted adjustable rate mortgages with teasers. No matter how high the Fed pushed rates, lenders could offer “option rate” deals in which borrowers would pay a rate of 1 or 2 percent for two to three years, after which there would be a huge reset. Lenders ensured the borrowers that there was no reason to worry about resets, since they would refinance into another option rate mortgage before the reset. That is the beauty of ARMs—they virtually eliminate the impact of monetary policy on real estate.

Second, and this was the key, house prices would only go up. At the time of refinance, the borrower would have far more equity in the home, thus obtain a better mortgage. Further, the borrower could flip the house and walk away with cash. While I will not go into this now, public policy actually encouraged homeowners to look at their houses as assets, rather than as homes (see here) (And now that many are walking away from underwater mortgages—treating houses as assets that became bad deals—policy makers and banksters are shocked, shocked!, that borrowers are treating their homes as nothing but bad assets.)

In truth, when speculation comes to dominate an asset class, there is no interest rate hike that can kill a bubble. If one expects asset prices to rise by 20%, 30%, or more per year, an interest rate of 10% will not dampen enthusiasm. To kill the housing boom, the Fed would have had to engage in a Volcker-like double-digit rate hike (in the early 1980s, he raised short-term interest rates above 20%). There was no political will in Washington (either at the Fed or the White House) for such drastic measures. Nor was there any reason to do this. Bernanke is quite correct: the Fed could have and should have killed the real estate boom with much less pain by directly clamping down on lenders, prohibiting the dangerous practices that were rampant.

Is there any reason to believe that Bernanke is the right Chairman, or that the Fed is the right institution, to lead the effort to re-regulate and re-supervise the financial sector? Quite simply, no.

The Bernanke-led Fed still does not understand monetary operations, as indicated by its recently announced plan to unwind its balance sheet. Over the course of the crisis, the Fed invented new procedures such as auctions through which it provided reserves. Throughout, it always was focused on quantities, rather than prices, using quantitative constraints on the size of the auctions. Further, Bernanke continually promoted “quantitative easing”, reflecting the view that quantities are what matter. Now, the Fed has begun to worry about the size of its balance sheet—and also the size of reserve holdings of the banking system (the other side of the balance sheet coin, because the Fed buys assets by issuing reserves). Still following the thoroughly discredited theory of Milton Friedman, too many bank reserves are supposed to promote too much lending which then causes too much spending and hence inflation. Thus, Bernanke and many outside the Fed fret about how the Fed can reduce outstanding reserves to prevent incipient inflation. The Fed proposes to create new bonds it will sell to reverse the “quantitative easing”.

Actually, the Fed’s tool is price, not quantity, of reserves. When the crisis hit, the Fed should have opened its discount window to lend reserves without limit, to all comers, and without collateral. That is how you stop a run. The Fed’s dallying and dillying about worsened the liquidity crisis, but it eventually provided the reserves that the financial institutions wanted to hold and its balance sheet eventually grew to $2 trillion. Banks are still worried about counterparty risk and possible runs, so they remain willing to hold massive amounts of reserves. When they decide risks have declined, they will begin to reduce reserve holdings. This will not require any special practices by the Fed. Banks will repay their loans from the Fed, using reserves. This automatically reduces reserves and the size of the Fed’s balance sheet. They will offer undesired reserves in the overnight, fed funds market. Since many banks will be trying to unload reserves at the same time, this will put downward pressure on the fed funds rate. The Fed will then offer to sell assets it is holding to mop up the excess reserves (banks will use reserves to buy assets the Fed offers). This will also reduce reserves and the size of the Fed’s balance sheet. All of this will happen automatically, following the same procedures the Fed has always followed. All it needs to do is to watch the fed funds rate, and when it falls below target the Fed will drain reserves to relieve the downward pressure on overnight rates.

Quantitative easing was a misguided notion, and reversal of quantitative easing is similarly misguided. It simply indicates that Bernanke still does not understand how the Fed operates. In truth, formulating and implementing monetary policy is extremely simple and can be reduced to the following:

1. Offer to lend reserves at the discount window at 50 basis points to all qualifying institutions;

2. Pay 25 basis points on reserve holdings;

3. Perform par clearing of checks between banks, and for the Treasury.

Surely President Obama can find a chair who can do that.

The Fed’s relationship with banks is too cozy to make it a good regulator. It is, after all, owned by private banks. The Fed’s district banks are often run by bankers, and district Fed presidents take turns sitting on the policy-making FOMC. There is a particularly incestuous relationship between the NYFed and Wall Street banks—with Timmy Geithner as a prime example of the dangers posed (“I’ve never been a regulator” proclaimed the former head of the NYFed). It does not have the proper culture to closely supervise financial institutions. Its top body, the Board of Governors, are political appointees often with no experience in regulation (many are academic economists, typically mainstream and with a free market orientation). While the FDIC was also mostly asleep at the wheel over the past decade, it does have the proper culture and experience to take over responsibility for regulating and supervising the financial sector. With some management changes, and hiring of a team of criminologists tasked to pursue fraud, the FDIC is the right institution for this job.

By Warren Mosler*

Fixing the Small Banks

First, the answer:

1. The Fed should loan fed funds (unsecured) in unlimited quantities to all member banks.

2. The regulators should then drop all requirements that a % of bank funding be ‘retail’ deposits.

The primary reason for the high cost of funds is the requirement for ‘retail deposits’ that causes the banks to compete for a finite amount of available deposits in this ‘category.’ While, operationally, loans create deposits, and there are always exactly enough deposits to fund all loans, there are some leakages. These include cash in circulation, the fact that some banks, particularly large, money center banks, have excess retail deposits, and a few other ‘operating factors.’ This causes small banks to bid up the price of retail deposits in the broker CD markets and raise the cost of funds for all of them, with any bank considered even remotely ‘weak’ paying even higher rates, even though its deposits are fully FDIC insured. Additionally, small banks are driven to open expensive branches that can add over 1% to a bank’s true marginal cost of funds, to attempt to attract retail deposits. So by driving small banks to compete for a limited and difficult to access source of funding the regulators have effectively raised the cost of funds for small banks.

It should be clear my solution would immediately lower the marginal cost of funds for small banks. I’ll now attempt to address the usual host of objections to my proposal.

There are always two fundamentals to keep in mind when contemplating banking with a non convertible currency and floating exchange rate:

1. The liability side of banking is not the place for market discipline.

2. The Fed and monetary policy in general is about prices (interest rates) and not quantities.

Disciplining banks on the liability side has been tried repeatedly and always and necessarily fails. First, it’s fundamentally impractical to the point of ridiculous to expect anyone looking to open a checking account or savings account, for example, to be responsible for analyzing the finances of competing banks for solvency, when even Wall Street analysts can’t reliably do this. The US leaned this the hard way when the banking system was closed in 1934, reopening with Federal deposit insurance for bank deposits for the sole purpose of removing this responsibility from the market place. Regulation and supervision on the asset side then became the imperative. And while we have seen periodic failures due to lax regulation and supervision of the asset side of the US banking system, and it’s a work in progress, the alternative of using the liability side of banking for market discipline exposes the real economy to far more disruptions and far more destructive systemic risk.

Those who understand reserve accounting and monetary operations, including those directly involved in monetary operations at the world’s central banks, have known for decades that in banking, causation runs from loans to deposits, with reserve requirements, if any, being merely a ‘residual overdraft’ at the central bank and not a control variable. This includes Professor Charles Goodhart at the Bank of England, who has written extensively on this subject for roughly half a century, endlessly debating the ‘monetarist’ academic economists who spew gold standard and fixed exchange rate rhetoric, and who are unaware of how monetary operations are altered when there is no legal convertibility of a currency. Recall the ‘500 billion euro day’ back in 2008 when the ECB added that many euro in reserves to its banking system, and a week later the monetarists pouring over the data ‘couldn’t find it.’ The fact that they even looked was evidence enough they had no actual knowledge of reserve accounting and monetary operations. And, more recently, the notion that ‘quantitative easing’ makes any difference at all apart from changes in interest rates (it’s always about price and not quantity) reinforces the point that there is very little understanding of monetary operations and reserve accounting. While Professor Goodhart did declare quantitative easing in the UK a ‘success’ he did so on the basis of how it restored ‘confidence,’ making it clear that there was no actual monetary channel of causation from excess reserves to lending. Banks do not ‘lend out’ reserves. Loans create their own deposits. Total reserves are not diminished by lending. This is operational and accounting fact, and not theory or philosophy.

What this means in relation to my proposal of unlimited lending by the Fed to small banks at its target rate, is that any lending by the Fed will not alter anything regarding lending and the ‘real economy’ in any other regard, apart from the resulting term structure of interests per se. (Also, and not that it matters in any event, total lending by the Fed won’t exceed funds ‘hoarded’ by some banks along with the usual operating factors that routinely ‘drain’ reserves.)

In other words, the notion that this policy will somehow result in some inflationary monetarist type expansion is entirely inapplicable with a non convertible currency and floating exchange rate policy.

The other common concern is the risk to the Fed of lending unsecured to its member banks. However, there is none, if you look at government from the macro level. All bank assets are already regulated and supervised, and the banks are continually subjected to solvency tests. This means government has already deemed to the banks ‘safe to lend to.’ Furthermore, functionally, the fact that banks can indeed fund themselves in unlimited size with FDIC insured deposits means the government already lends to banks in unlimited quantities, protecting itself by regulating and supervising the assets, including asset quality, capital requirements, etc. Therefore, the Fed asking for collateral from its member banks is entirely redundant, as well as disruptive and a cause of increased rates to borrowers.

Conclusion: If the Obama administration had the knowledge, they would immediately move to implement my proposals to support small banking.

*First published on Moslereconomics.com

Click images to view details