The Sector Financial Balances Model:

Domestic Private Balance + Domestic Government Balance + Foreign Balance = 0

is an accounting identity that provides a focus for macroeconomic analysis, explanation, and prediction by economists applying the Modern Money Theory (MMT) approach. It leads to a very critical line of thinking about the budget deficit projections produced for our consumption by the Congressional Progressive Caucus (CPC), Congressional Budget Office (CBO), the House, and the Senate. The US has recently had a sharp decline in its balance of trade deficit. It now stands at about 3% of GDP; which means that the rest of the world has a surplus, a balance of +3% of US GDP in its annual trade with the United States.

Assuming that surplus is unlikely to shrink anymore, we can see from the equation that unless the Government balance is less than -3% of GDP, the Domestic Private Balance in the United States economy will not be positive (a surplus, and addition to nominal financial wealth) and is very likely to be negative (a deficit, a subtraction from nominal financial wealth). So, the private sector taken as a whole will be losing rather than gaining Net Financial Assets (NFAs), every year for as long as the situation lasts.

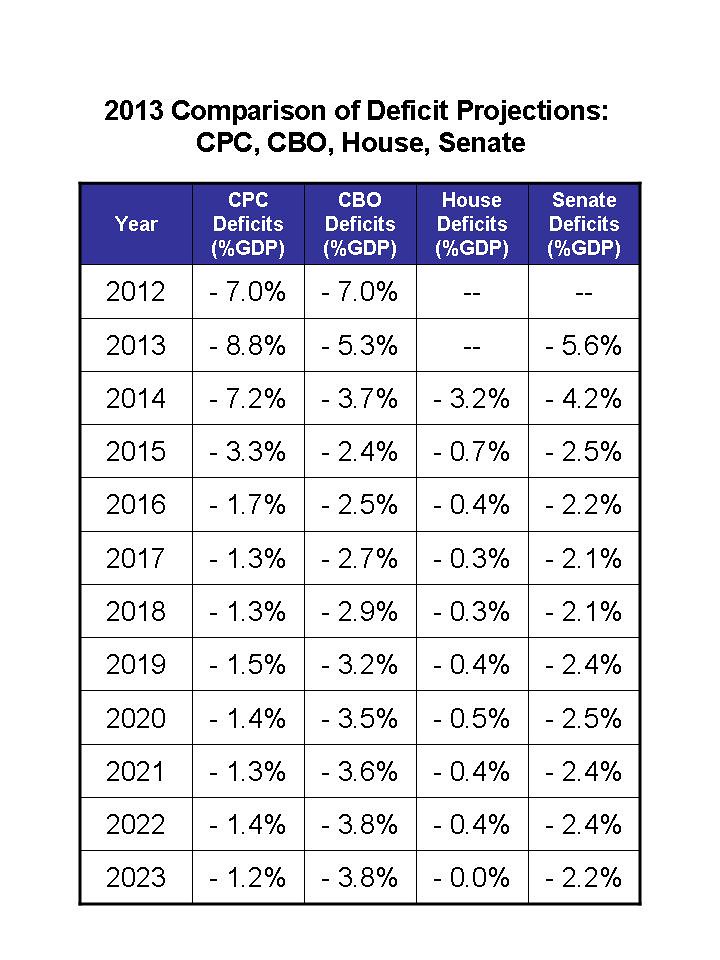

The Table below presents the CPC, CBO, House and Senate budget projections through 2023.

The CBO projections are worse than CPC’s from 2013 – 2015; but thereafter, its larger deficits are less damaging to aggregate demand than the CPC’s deficits. But they are not large enough to provide for anything but economic stagnation, unless, again, there’s a credit bubble, which would then mean a crash from mere stagnation somewhere down the line.

Of course, the most austerity-filled plan of the four is Paul Ryan’s House Budget which begins its projections in 2014 with a deficit slightly above 3.0%, and then quickly arrives at minimal deficits ending in a balanced budget projection for 2023. If these projections were enforced through an activist Government policy, and the trade balance did not move towards a US trade surplus, then we would have declines of private sector NFAs ranging from 2.3% to 3.0% of GDP every year from 2015 through 2023. There’s no way that course would persist until 2023. But if it did, then nominal financial wealth in the private sector would decline by about 28% of nominal GDP over that period.

I can’t predict when this continuous decline in private sector NFAs would result in another financial crash and great recession/depression, because the banking system can blow new credit bubbles sustaining “paper” growth for some years if it wants to. But eventually, without increasing private sector NFAs to sustain such a bubble, a new crash would surely occur. My guess would be that if anything like the Ryan Budget were passed, then the next crash would come within a five year time frame.

The last of the four budgets whose deficit projections are included in the table is Patty Murray’s Senate Budget. It’s very similar to the CBO projections for 2013 – 2015, providing little space for private savings. From 2016 – 2023, this budget projection provides less space for private sector savings than CBO’s projection, which itself is far from expansionary, but more than both the CPC budget, and Paul Ryan’s House budget during those years.

So, the bottom line here is that all four of these budget projections, if implemented could only correspond to a bleak, stagnating economic future for the United States, with the House Budget producing the worst result by far. I’m sure this analysis would be strongly objected to by the authors of all four budgets. But of the four, the most credible claims against what I’ve written would probably come from CPC neo-keynesian budget proponents.

They’d claim that the back-to-work 1.4 T and 1.2 T of deficit spending their budget plan envisions for 2013 and 2014, would bring the economy back to much lower unemployment levels, so that by 2015, increasing tax revenues would support reductions in deficit spending projected for later years without austerity. In making a claim like this, however, the CPC would only be exhibiting its own lack of understanding of the Sector Financial Balances model, and the constraints on the economy it implies.

Let’s grant that the back-to-work budget works to create enough new jobs by the end of 2014 to bring the U-3 unemployment rate down to 5%, so that tax revenues have made a big comeback by 2015. Then the SFB model still applies, so that if the deficit goes down to 3.3% as projected for 2015, and given the foreign balance of 3%, then there will be only a fraction of a percent in overall addition to private sector nominal financial wealth, which taking even a low rate of inflation into account, would actually represent a decline in inflation-adjusted nominal financial wealth.

There might well be less than that if increasing demand in 2013 and 2014 leads to a growth in the foreign balance to 4% in 2014 – 2015. If that happens, then private sector savings would be underwater by 2015, and way underwater if the CPC budget course were somehow maintained into later years. Again, we could expect domestic private sector savings losses from 2016 on, and even perhaps in 2015. We could not have too many years of those without hitting another great recession. So, the CPC budget may be better than the others for a couple of years, but the danger in it is that the CPC will take it seriously and, assuming its success in the first two years, would then push forward on the budget course projected, deterred eventually only by the inevitable crash, which hopefully would occur in very short order, rather than being postponed by another credit bubble, only to be even more severe later on.

Moving to all four budgets, I want to emphasize that apart from the above macroeconomic considerations and their significance for declining domestic private sector wealth over time, the situation looks even worse when we take economic and political power considerations and their likely effect on the economy into account. The history of the US since 1970 shows clearly that when the private sector gets a cold, the household sector gets pneumonia.

Big businesses, the financial sector, and wealthy oligarchs will use their economic and political power to see to it that their nominal financial wealth will continue to increase even as the private sector as a whole is losing 20% – 30% of its financial wealth. Over the period of a decade, that will exacerbate the already ridiculous level of inequality we see in American society, and accelerate the movement toward plutocracy in America if we allow any of these austerity plans, or any variations between the CPC proposal and the House proposal to be passed and implemented.

So, where are we with these budgets? I think they’re all illustrations in fiscal fantasy, or perhaps I should say, in fiscal science fiction using bad fiscal science. In taking a fiscal approach based on reducing budget deficits, all the budgets are doing the wrong thing for the economy and the wrong thing for America. The right approach to take to fiscal policy is to design and implement programs that will guarantee full employment at a living wage for everyone who wants to work full time and is able to do so.

If the government does that, then it will let the domestic private sector determine what both the foreign balance and the domestic private sector balance should be. Then these sector balances would drive the government balance. That balance could be a surplus or a deficit of a particular size, though in the case of the United States it would probably be a large deficit, or, as I prefer to call it, a large Government addition, to domestic private sector wealth, for some years to come. But it would be determined by the wishes of those in the domestic private sector, with the Government’s role being one of accommodating the surpluses or deficits.

Seeing this conclusion, I’m sure that some of my readers will ask: how can the United States afford to run deficit after deficit while continuing to accumulate its national debt? Well, first, it doesn’t have to accumulate and can even pay off its national debt without inflation. I’ve explained how it can do that in my new e-book on Fixing the Debt without Breaking America. But second, even if the US does the politically unwise thing of continuing to accumulate a larger and larger national debt, it can do that without either solvency or inflation problems. Scott Fullwiler has done a very good job of explaining how that can happen in a recent series of his, which concludes here.

So, it turns out that deficits can be run indefinitely by nations with non-convertible, fiat currencies, with floating exchange rates, and no external debts in currencies not their own, without either solvency or inflation problems as long as the Government doesn’t deficit spend beyond full employment. That’s the kind of fiscal policy we should be making, not fiscal policy deliberately aimed at deficit reduction. So, to all the fiscal budgeteers in Washington looking to implement long-term plans for deficit reduction: a plague on all your budgets. You’re ending America, as we’ve known it!

Pingback: A Plague on All Your Budgets | Real Economy & Geopolitics | Scoop.it