By Philip Pilkington

(Cross posted from Fixing The Economists)

Piketty’s Wikipedia page says that he’s a Keynesian. Well, I don’t see it at all. His book contains a section on the public debt in historical perspective and it is desperately misinformed.

Piketty’s Wikipedia page says that he’s a Keynesian. Well, I don’t see it at all. His book contains a section on the public debt in historical perspective and it is desperately misinformed.

A caveat first though: I actually like Piketty’s book in a lot of ways. While not extremely well written, it is highly readable (if you are an historical data sort of person). And it is very nice to see what is effectively a work of economic history get so much play. Because economists should be far more interested in reality than in modelling and this book could spur that interest.

But the history presented in Piketty’s book is selective and, I think, ultimately untrustworthy. Even the way he chooses to present data — both in terms of the averaging of the time periods and aggregates used — is often quite misleading. I don’t want to get too far into this here but I’m pretty concerned that people who are broadly ignorant about economic history are reading this book and coming away, in many ways, misinformed.

Anyway, let’s deal here with one issue; namely, that of how Piketty treats the public debt. He discusses two countries: Britain and France. Both of these countries ran up massive debts in their late-18th century wars (mainly with each other!). France pretty much cleaned its slate during the French Revolution through a combination of partial default and sustained inflation. But Britain carried its debt into the 19th century.

Piketty takes a sort of crude socialist view of the debt as a tax on society. He sees it — as Marx did too, mind you — as a means to redistribute money by taxing goods and services bought by workers in order to pay rich rentiers. He tells us, for example, that in Britain the owners of the debt were obtaining fairly high interest payments. I don’t really see the rates of interest in these years as being particularly high. They basically fluctuated just below the 5% mark.

Frankly, I’m a bit wary of Piketty’s interpretation of the taxation system in this time period. He seems to hold a very narrow view in that he seems to think that the taxation system is merely a means by which redistribution takes place and in this period that redistribution is from poor workers to rich debt holders. While this is one function of the taxation system, it is not the only one. But in this chapter Piketty pretends that it is. This is altogether not very Keynesian.

He also notes that Britain had fiscal surpluses throughout this era.

For an entire century, from 1815 to 1914, the British budget was always in substantial primary surplus: in other words, tax revenues always exceeded expenditures by several percent of GDP—an amount greater, for example, than the total expenditure on education throughout this period. (p200)

Piketty views this from the perspective of rentiers sucking wealth from the population in the form of taxes. In some sense this might be true — although I really doubt that interest payments on government debt were a key component of inequality in 19th century Britain, as any cursory reading of the history of the industrial revolution will confirm. But I suspect it is misleading in terms of the wider picture. In fact, Britain was very likely running a budget surplus in this era because, being the workshop of the world and penetrating colonial markets, it was running large trade surpluses (Piketty notes this elsewhere in the book but fails to make the connection).

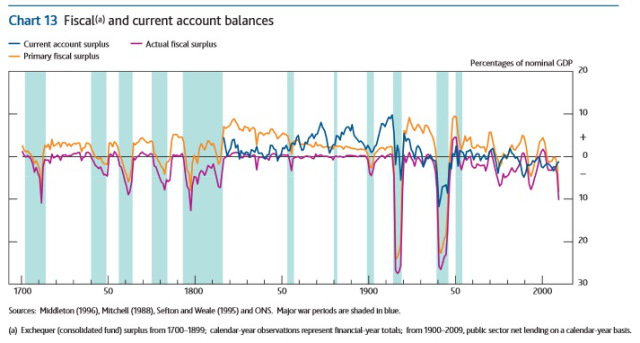

Update: Phillipe has kindly linked to a Bank of England paper in the comments section entitled The UK recession in context — what do three centuries of data tell us?. It provides us with the data on the current account and the public fiscal balance for this period. As can be seen from the graph below the current account was indeed in substantial surplus for the entire 19th century. This was probably the main component of the fiscal surplus, just as simple logical deduction would lead us to assume.

At the same time the Industrial Revolution was roaring and the private sector was probably investing heavily. Thus it is not a big surprise that the government was running a budget surplus for much of the 19th century. After all, that is what the sectoral balances identity would tell us. And since unemployment was very low in this era the combination of a large export surplus and high domestic investment probably required the public sector to run a surplus. Yes, the tax could have been imposed on, say capital gains, rather than on workers, but come on… this was 19th century England!

This sets the stage for the moral tone that Piketty takes with regards to the public debt for the rest of the section. He notes that it is inflation which kept the public debt levels down in the 20th century — even when they spiked after wars. He seems to equate this with the borderline hyperinflation initiated by the Jacobins and thinks of it as a sort of partial default. I think that this is deeply misleading.

In fact, people who hold government debt are used to such levels of inflation — Piketty is, after all, only talking about an average rate of 3% inflation a year in the era spanning from 1913-1950. This leads him to come out sounding like an Austrian warning about the impending doom if some inflation is maintained. I will quote him in the original here:

Second, the inflation mechanism cannot work indefinitely. Once inflation becomes permanent, lenders will demand a higher nominal interest rate, and the higher price will not have the desired effects. Furthermore, high inflation tends to accelerate constantly, and once the process is under way, its consequences can be difficult to master: some social groups saw their incomes rise considerably, while others did not. It was in the late 1970s—a decade marked by a mix of inflation, rising unemployment, and relative economic stagnation (“stagflation”)—that a new consensus formed around the idea of low inflation. (p203)

There’s lots of this sort of unsophisticated stuff in Piketty’s book. And it seems to me likely that this is because, in some ways, the book is a mess owing to a lack of a solid macroeconomic framework. I only take the example of public debt because I know that many of my readers will be all to familiar with this silliness and will be immunised against such thinking.

The more I read Piketty the more I see him as synonymous with the Hollande government in France; proposing taxes at a time when these would ruin the economy while maintaining very mainstream opinions on the role of the public debt in the economy.

Again, I like Piketty’s book overall but I really don’t think his macroeconomic credentials are up-to-scratch. This leads to a lot of silly sections and a lot of misleading interpretations. If you’re not fairly familiar with economic history and don’t have a good grasp of basic macroeconomic principles, I suggest that you handle this book with care. I suppose that warning would apply to the vast majority of working economists too. And for that reason I find it very unlikely that Piketty’s book will have much of a theoretical impact.

Much more likely that various people will cast various contradictory interpretations of the accounting identities that Piketty refers to, rather grandiosely, as ‘laws’. Thus, Piketty’s should be seen as one of those books that will open discussion on a topic without much contributing to it. His accounting identities — like the r > g identity — provide a sort of blank screen upon which commentators will be able to project whatever theory they have concocted with regard to the cause of inequality.

This will likely give rise to an academic industry ruminating on such questions — indeed, such already seems to be taking place and I think that it is the exodus of major figures like Krugman into this new land that has led to the media hype surrounding Piketty’s book (even academics do PR!).

For those of us interested in the study of inequality this is wonderful. Although expect a debate that has been taking place behind the scenes in a very focused manner to quickly become filled with sludge as every crackpot economist puts forward their little model explaining, in one fell swoop, the rise of income inequality while simultaneously handing us the silver bullet to rid us of it.

3 responses to “Piketty’s Regressive Views on Public Debt and the Potential Impact of His Book”