By Stephanie Kelton

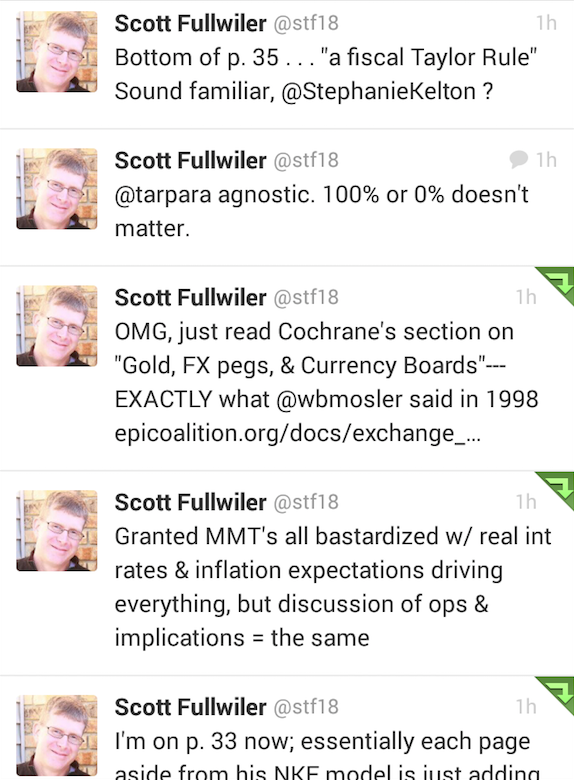

Scott Fullwiler spent part of the afternoon reading (and reacting to) a paper that John Cochrane just gave at a conference on central banking in Stanford, CA. I haven’t read the paper yet, but judging by Scott’s reaction on Twitter, there’s lots to like about it. (Mostly because it appears to draw heavily from a broad swath of at least a decade of published work from MMTers.)

We’ll have to wait for Scott’s forthcoming post to see just how close the parallels are (and how much Cochrane 2014 departs from Cochrane 2009). It will be interesting, particularly because several years ago Cochrane wasn’t interested in garnering insight from outside the mainstream. “Every now and then,” he confessed, “there’s an excluded subgroup that turns out to be right.” But he readily admitted — nay, disparaged — “I haven’t read their specific work. I’m busy, and I try to read what is considered interesting and valid.” Being right matters, and I think that’s why MMT has begun to seep into the mainstream. The risk (though this is not how Noah sees it) is that “all the interesting heterodox ideas [will] quickly get incorporated into the mainstream in some slightly bastardized form,” leaving the discipline as a whole only marginally better off, while those who did the heavy lifting remain at the margins.