My piece last week on MMT for Austrians set off a bit of aflurry of comments here and across the web, aided and abetted by commentary onthe MMT event in Italy. Several followers of NEP have asked us to respond tosome of the critiques made against MMT. I think that a long response iscalled-for, something we will put on both NEP and MMP as a blog. I’m ignoringthe various Austrian comments over at Naked Capitalist—as my colleague Bill Blackalready offered thoughts. Besides, most of the commentary there is notsubstantial enough to require a response— given the constraints imposed oncommentary on blogs, there’s not a whole lot there to respond to even in theposts by “reasonable” people.

I’m instead going to (mostly) respond to a series ofcomments made by reporter John Carney. I want to be clear here. This is notbecause Carney has made the most outrageous statements, but precisely theopposite: he has provided the most thoughtful reactions. And Carney understandsMMT; indeed, he accepts much of the exposition. Further, as Carney is areporter, he is not wont to making undocumented claims. Reporters know how todo “fact checking” and are held to much higher standards than are bloggers whohide their names and thus are free to make any outlandish claim they want. Ipresume that when Carney writes articles for CNBC the standards are higher thanwhen he writes for his own blog at CNBC. Still, as a reporter his reputationand credibility would be severely damaged if he were to make unsubstantiatedclaims—so I presume he has fact checked his claims.

I’m going to rely on his “published” (that is to say, postedon internet sites, mostly his own) comments, plus a tweet or two (whatever thatis).

There are three main themes. First, there is areinterpretation of what we call sectoral balances, with a restatement andclaimed correction to the MMT approach. Second, there is a claim that MMT doesnot account for corruption in government. And finally his main critiqueconcerns the role of government—what shouldgovernment do. There is something approaching a blanket claim that governmentcan only impose economic costs—its positive contribution approaches zero. Hence,he appears to reject my whole premise that while we can agree on MMT asdescriptive, reasonable people can disagree on the “public purpose”—whatgovernment ought to do.

For Carney there is no such thing as a public purpose, andhence no positive role for government to play. Reasonable people cannot agree to disagree on the publicpurpose because the concept is rejected.

Let me repeat: I am using Carney’s posts because I thinkthey are the most cogent critiques the Austrians have to offer.

If we cannot effectively defend the MMT position againstCarney’s critiques, then—as he claims—we at NEP “are doing something else that maybe interesting but it isn’t economics. It isn’t a new economic perspective orheterodox economics or any kind of economics at all.”

That is quite a claim for a reporter to make—we at NEP donot do any kind of economics at all. Let’s see if he’s got his facts checked.

Theme One. From a Tweet: JohnCarney@carney: “Blows my mind when MMT people say that”accounting identities” prove that people can’t save without gov’t orfor[eign] sect[or] running a deficit.”

Moi? Said people?Can’t save? Without government or foreign deficit? Really? We saidthat?

No John, we neversaid that. If any true MMTer ever said that it was in some special context.Here is what we actually say.

From MMP Blog #2: Insidewealth vs outside wealth. It is often useful to distinguish among types ofsectors in the economy. The most basic distinction is between the public sector(including all levels of government) and the private sector (includinghouseholds and firms). If we were to take all of the privately-issued financialassets and liabilities, it is a matter of logic that the sum of financialassets must equal the sum of financial liabilities. In other words, netfinancial wealth would have to be zero if we consider only private sector IOUs.This is sometimes called “inside wealth” because it is “inside” the privatesector. In order for the private sector to accumulate net financial wealth, itmust be in the form of “outside wealth”, that is, financial claims on anothersector. Given our basic division between the public sector and the privatesector, the outside financial wealth takes the form of government IOUs. Theprivate sector holds government currency (including coins and paper currency)as well as the full range of government bonds (short term bills, longermaturity bonds) as net financial assets, a portion of its positive net wealth…..Wecan formulate a resulting “dilemma”: in our two sector model it is impossiblefor both the public sector and the private sector to run surpluses. And if thepublic sector were to run surpluses, by identity the private sector would haveto run deficits. If the public sector were to run sufficient surpluses toretire all its outstanding debt, by identity the private sector would runequivalent deficits, running down its net financial wealth until it reachedzero.

OK, if you read no further than this, it might seem to lenda tiny bit of support to Carney’s claim. Note however the words used are “privatesector”, not “people”. So if one has a problem with the logic of this passage, Ido not know what the heck it is: Two sectors. One can spend less than onesincome only if another spends more. Surely any Austrian can understand this? IndeedJohn, later, seems to state exactly this:

Carney: The only thingthat can make private-sector net savings possible is government spending. Ifthe government spends more than it takes in taxes, the private sector can earnmore than it spends. Remember, if everyone pays less than they earn, some outsidermust be paying more than he earns. The government is basically filling in therole of the family who constantly needs babysitting—using up those saved hoursand, therefore, providing a chance for the shut-in Park Slope parents to saveeven more hours. Once you wrap your head around that, it seems easy tounderstand what those MMT people are talking about when they say the governmentmust run a deficit in order for the private sector to net save. But it’s alsoeasy to mistake this fact for a number of similar but false statements.

Well, except for putting it in babysitter terms, John seemsto argue exactly what I said above, written in Blog 2 early last summer.

So let us now go further. Let us separate “people” from“firms”, the sum of which is “private sector”. Are MMTers confused on how to doa simple division by the number two? Yes, John thinks we are incapable of suchmath. And to be fair to John, there is a whole website, called MMR, devoted tothis supposed confusion on the part of MMT. I’ll come back to the MMR confusionin a second.

Here is Carney’s claim:

Carney: The recentblogosphere kerfuffle about saving arose in part because MMT embraces thesector financial balances model (SFB), which features the consolidation ofhousehold and corporate sectors as a unified private sector. The model treatsfinancial claims on corporations as negative financial assets for corporations,so the consolidated result is that household saving deployed in such financialassets makes a zero net contribution to private sector saving aftercounterparty corporate netting….

First let’s see what I actually wrote last summer. John,here it is, you can read it for yourself (I’ve done your fact checking foryou!):

MMP Blog #4: Deficits in one sector create thesurpluses of another. Earlier weshowed that the deficits of one sector are by identity equal to the sum of thesurplus balances of the other sector(s). If we divide the economy into threesectors (domestic private sector, domestic government sector, and foreignsector), then if one sector runs a deficit at least one other must run a surplus.Just as in the case of our analysis of individual balances, it “takes two totango” in the sense that one sector cannot run a deficit if no other sectorwill run a surplus. Equivalently, we can say that one sector cannot issue debtif no other sector is willing to accumulate the debt instruments. Of course,much of the debt issued within a sector will be held by others in the samesector. For example, if we look at the finances of the private domestic sectorwe will find that most business debt is held by domestic firms and households.In the terminology we introduced earlier, this is “inside debt” of those firmsand households that run budget deficits, held as “inside wealth” by thosehouseholds and firms that run budget surpluses. However, if the domesticprivate sector taken as a whole spends more than its income, it must issue“outside debt” held as “outside wealth” by at least one of the other twosectors (domestic government sector and foreign sector).

So, can Wray dodivision by two without confusion? Looks like he can. Even with a governmentbudget that is balanced (and a foreign sector balance) it is possible forhouseholds to net save!

Wow!

And it is possiblefor Carney to save while Wray deficit spends—even though we are in the samehousehold sector! In other words, even the household sector can be balanced andCarney—one of those households—can net save!

So, even if firmstaken as a whole are balanced, and the government is balanced, and the foreignsector is balanced, one household can net save while another deficit spends!(Note we can subdivide the private sector as many times as we want and stillderive similar results.)

And if John thinksthat I just discovered these ideas last summer (maybe after reading the“brilliant” analysis by JKH—see below), he can look at my 1998 book, Understanding Modern Money (to myknowledge, the first time “modern money” was used to describe the MMTapproach), Chapter 4, page 82 for almost exactly the same explanation—“To simplify we can assume that it is thehousehold sector which saves and the business sector that invests; the net(inside) indebtedness of the business sector is exactly offset by the net(inside) financial wealth of the household sector. It is frequently the casethat the household sector wishes to save more than the business sector wishesto invest.” And so on and so on and so on.

We didn’t even needthe MMR blogsite! MMTers had it right all along!

And we really don’teven need Carney’s babysitter model, where he tries to correct MMTers with thefollowing explanation:

Carney: Theway Modern Monetary Theory folks talk about the economy leads to a lot ofconfusion. The best example is the assertion that the private sector cannot”net save” unless the government runs a budget deficit. This annoysand confuses people because it seems to be an assertion that people cannot savemoney unless the government is running a deficit. If that was what MMT wasclaiming, it would be nonsense. You and I are perfectly capable of savingregardless of how the government’s spending and revenues balance out

John claims MMT“seems” to say “people” cannot “save money”? Why would it “seem” such? MMT seemsto me to say exactly the opposite of that? If John is “annoyed” I guess it isbecause he is not bothering to read what we actually write?

Now, John, if youwant to say that you are a much better writer than me, fine. Go for it. Maybewhat I write is beyond the grasp of the typical MMR blogger. I can rememberwhen many people claimed that a certain MMR blogger was a much better writer thananyone at NEP and thus much better able to explain MMT—(only to find later thathe rejects most of MMT and misunderstands much of it. Another matter entirely,admittedly. Sorry for the sidetrack.).

And if Carney andMMR were correct about the three balances, then that means Wynne Godley has tobe wrong. I worked with Wynne and unlike the MMR folks I published with him (wewere the first, ever, to warn of the coming global financial collapse,beginning in 1998). And I taught him MMT. He began to write a“government-centered” textbook, beginning with “taxes drive money” from ChapterOne. Unfortunately, he did not live to see that book come to fruition, but hedid incorporate much of the ideas into his analysis. And all of us MMTers owe agreat debt of gratitude to Wynne for helping us to understand the threebalances.

Carney: The problem here is that the correctdefinition of saving precisely specifies the passive act of not spending onconsumer goods. It does not specify how the proceeds of such saving should beused, whether to acquire real or financial assets. Saving is described inproper accounting terms as funds sourced from income by virtue of being savedfrom income. The eventual deployment of that source of funds is described properlyas a use of funds — whether such deployment and use occurs in the form of abank deposit, a bond, a stock, newly produced residential real estate, or newlyproduced plant and equipment. The deployment or use of funds is separate fromthe act of saving itself. In summary, the consolidated private sector accountobscures, not only the view of saving as it materializes within a givenaccounting period in bifurcated fashion across household and corporate sectorsseparately, but also the view of total private sector saving as it is projectedfully into the household balance sheet, when captured as a cumulative measureover a sequence of such accounting periods. As a result, the consolidatedprivate sector presentation within the sector financial balances model obscuresthe measurement of the core component of saving.

So, MMT does not getinto what the savings are used for? Let us see what I wrote:

MMP BLOG #21:GOVERNMENT BUDGET DEFICITS AND THE “TWO-STEP” PROCESS OF SAVING. … as J.M. Keynes argued, saving is actually atwo-step process: given income, how much will be saved; and then given saving,in what form will it be held…. How can we be sure that the budget deficit thatgenerates accumulation of claims on government will be consistent withportfolio preferences, even if the final saving position of the nongovernmentsector is consistent with saving desires? The answer is that interest rates(and thus asset prices) adjust to ensure that the nongovernment sector is happyto hold its saving in the existing set of assets.

{Now there are a lotof different definitions of the term “saving”. I actually wrote a journalarticle on that (it is short and not too wonky: “What is Saving, and WhoGets the Credit (Blame)?”, Journal of Economic Issues, vol. 26,no.1, March 1992, pp. 256-262). To briefly summarize, at NEP we prefer to usethe Godley sectoral balance approach, where he defined private sector saving as“net accumulation of financial assets” (NAFA), using the flow of funds data. Typicallyeconomists use the GDP equals national income equation where saving is definedas a residual: the net income received but not consumed (I’ll use it below indiscussing the MMR approach). In theory these would lead to approximately thesame result; in practice they do not because the NIPA accounts include imputedvalues. Godley preferred the flow of funds data but even they had to becarefully adjusted to ensure that every spending flow is actually financed andactually “goes somewhere” (ensuring “stock-flow consistency”). That is allquite wonky. My bigger point is that we can come up with alternativedefinitions of saving that would include unrealized capital gains as real andfinancial assets appreciate in value. Some want to include accumulation of realproduction—say, a farmer who produces corn for his family’s own consumption,who “saves” by putting away seed corn for future planting. All that is fine butas it does not have a financial counterpart it is not included in either theNAFA or NIPA definitions usually used in MMT. I’ll come back to this later.That should be clear in the quote above, which is discussing receipt of incomeand then a decision about how to save a portion of it so it has to be NAFA orNIPA saving, and not “real” saving of seed corn.}

Let’s get back toCarney’s complaints and “corrections” of MMT theory. Carney wants to go a bitfurther, moving on to causal relations among the balances to correct supposed MMTerrors. Here is his critique:

Carney:Also, it’s simply not true that government deficits result from the privatesector’s desire to net-save. Deficits can “accommodate” an aggregate demand inthe private sector to save more than it earns, but they don’t result from thatdemand. Deficits result from votes by politicians interacting with the realeconomy. There’s no “to the penny” causal relationship.

Oh, really? And soGreece and Ireland are imposing Austrian Austerity and finding that deficitsremain. Now why is that? Here is what I wrote (hint, you do not even need toread beyond the title of my post to get the drift of the argument):

MMP Blog #5: GovernmentBudget Deficits are Largely Nondiscretionary: the Case of the Great Recessionof 2007

In previous blogs we have examined the threebalances identity and established that the sum of deficits and surpluses acrossthe three sectors (domestic private, government, and foreign) must be zero. Wehave also attempted to say something about causation because it is not enoughto simply lay out identities. We have argued that while household incomelargely determines spending at the individual level, at the level of theeconomy as a whole it is best to reverse that causation: spending determinesincome. Individual households can certainly decide to spend less in order tosave more. But if all households were to try to spend less, this would reduceaggregate consumption and thus national income. Firms would reduce output,thus, would lay-off workers, cut the wage bill, and thereby lower householdincome. This is Keynes’s well-known “paradox of thrift”—trying to save more bycutting consumption will not increase saving…. In the aftermath of the globalfinancial crisis (GFC) social spending by government (for example, onunemployment compensations) has risen while tax revenues have collapsed. Thedeficit has grown rapidly leading to widespread fears of eventual insolvency orbankruptcy….. The implication of growing deficits has been attempts to cutspending (and perhaps to increase taxes) to reduce deficits. The national conversation(in the US, the UK, and Greece, for example) presumes that government budgetdeficits are discretionary. If only the government were to try hard enough, itcould slash its deficit. As I have argued in previous blogs (particularly inresponses to questions), however, anyone who proposes to cut governmentdeficits must be prepared to project impacts on the other balances (private andforeign) because by identity the budget deficit cannot be reduced unless theprivate sector surplus or the foreign surplus (flip side to the domesticcurrent account deficit) is reduced. In this blog, let us look at the rise ofthe US government budget deficit since the GFC hit. We will ask whether thedeficit has been, and might be, under discretionary control—if not then thatraises questions about the attempts by deficit hysterians to reduce deficits.

I’m not going torepeat the whole argument here. Carney’s view seems to be that Congress votedto raise the deficit and that is why it exploded. Nonsense. As I show in thatblog (that came out of an academic paper at www.levy.org) and as many of us atNEP have demonstrated, most of the increase to the US budget deficit was due tocollapse of tax revenue—and most of that was unrelated to the Bush tax cuts.There were no Congressional votes to increase the deficit to a trillion dollarsa year. There was a relatively small fiscal stimulus package that petered outover two years–$400 billion each. Deficits remain two years later and areorders of magnitude larger than the Congressionally-mandated stimulus packageplus tax cuts. Where is the legislation to pump up deficits?

John, please listthe changes to public law and the impacts of each on deficits; total theresults and you will not get close to the expansion of budget deficits. Andnote that most of the offsetting impact of the rise to government deficits wasin the domestic private sector—not on the foreign sector. In other words, the growinggovernment deficits were mostly offset by growing private surpluses.

Haven’t Americans triedto “net save” more as a result of the crisis? Didn’t they cut back on shopping?Or is it “just my imagination running away with me” (as the Stones might say)that makes me perceive slower sales and ramped up layoffs? Did 10 millionworkers suddenly decide to take extended vacations? Or did they lose their jobsdue to a rotten economy that encouraged consumers to cut back spending, whichlowered GDP, which lowered national income and tax receipts, which causedgovernment deficits to balloon?

On Carney’sreference to “to the penny causal relation”, that is not what MMTers haveargued. Rather, Warren Mosler has argued that in a two sector model, thegovernment sector deficit equals the nongovernment surplus “to the penny”; ifwe have three sectors then the government sector deficit equals the surplusthat represents the sum of the foreign and domestic private sector balances. Thecausation is more complicated, as we have always argued. Don’t believe me? Okhere is what I argued throughout the MMP: it takes “two to tango”, so causationis complex:

MMP Blog #4: Becausethe initiating cause of a budget deficit is a desire to spend more than income,the causation mostly goes from deficits to surpluses and from debt to netfinancial wealth. While we recognize that no sector can run a deficit unlessanother wants to run a surplus, this is not usually a problem because there isa propensity to net save financial assets. That is to say, there is a desire toaccumulate financial wealth—which by definition is somebody’s liability.

MMP Blog #20: Since tax revenues (and some governmentspending) are endogenously determined by the performance of the economy, thefiscal stance is at least partially determined endogenously; by the same token,the actual balance achieved by the nongovernment sector is endogenouslydetermined by income and saving propensities. By accounting identity it is notpossible for the nongovernment’s balance to differ from the government’sbalance (with the sign reversed—one has a deficit and the other a surplus);this also means it is impossible for the aggregate saving of the nongovernmentsector to be less than (or greater than) the budget deficit.

MMP Blog #4: Deficits -> savings anddebts -> wealth. We have established in our previous blogsthat the deficits of one sector must equal the surpluses of (at least) one ofthe other sectors. We have also established that the debts of one sector mustequal the financial wealth of (at least) one of the other sectors. So far, thisall follows from the principles of macro accounting. However, the economistwishes to say more than this, for like all scientists, economists areinterested in causation.Economics is a social science, that is, the science of extraordinarily complexsocial systems in which causation is never simple because economic phenomenaare subject to interdependence, hysteresis, cumulative causation, and so on.Still, we can say something about causal relationships among the flows andstocks that we have been discussing in the previous blogs…. If a household orfirm decides to spend more than its income (running a budget deficit), it canissue liabilities to finance purchases. These liabilities will be accumulatedas net financial wealth by another household, firm, or government that issaving (running a budget surplus). Of course, for this net financial wealthaccumulation to take place, we must have one household or firm willing todeficit spend, and another household, firm, or government willing to accumulatewealth in the form of the liabilities of that deficit spender. We can say that“it takes two to tango”…. We can suppose there is a propensity (or desire) to accumulate net financial wealth. Thisdoes not mean that every individual firm or household will be able to issuedebt so that it can deficit spend, but it does ensure that many firms andhouseholds will find willing holders of their debt. And in the case of asovereign government, there is a special power—the ability to tax–thatvirtually guarantees that households and firms will want to accumulate thegovernment’s debt…

The causation isdifficult. It takes at least two to tango—a deficit spender and a willing saverto accumulate claims on the spender. We can summarize it as: at the aggregatelevel, spending determines income. But government deficits are largelynondiscretionary, to some extent they “fill the gap” left by collapsing privatesector spending as government spending and taxing are largely countercyclical. Theother side of the collapsing private spending is the desire by the privatesector to repay debt and accumulate saving.

Let’s move toanother topic Carney raises regarding this issue.

Carney: This raises aninteresting question: should we enable the private sector to net save? There’sa good argument that we shouldn’t use government for this purpose. A privatesector that doesn’t have recourse to government savings accounts would likelyinvest more.

Hold on there. If government spending and taxing are in anyway tied to economic performance there is no intentional “enabling”required—the budget outcome will be countercyclical (deficit in bust, movingtoward surplus in boom). Now if what Carney wants is a fixed governmentspending (say, $100 per year) and a fixed head tax ($1 per capita per year oneach of the 100 inhabitants) then net spending by government will be zero solong as the inhabitants can actually pay their tax. It is far more likely thatsome will not be able to do so on a continuous basis, so the government willincur a deficit, and some taxpayers will lose their heads (penalty for notpaying the head tax).

Carney’s final statement that in the absence of a governmentdeficit, private saving would lead to more investment just makes no sense.Assume no government and no foreign sector. Investment creates saving in financial terms. Investment and Saving cannot beunequal. Add government that runs a deficit, then investment plus the deficitequals saving. Add the foreign sector and saving will equal the sum ofinvestment plus net exports and plus the government deficit. This is not aneither/or thing. It is an identity:

One Sector: I = S

Two Sectors: I + Def = S

Three Sectors: I + Def + NX = S

It is first day of economics 101. And there has been a longacademic tradition since Keynes’s GeneralTheory to establish the causation. In the one sector model, the causationmust run from investment to saving.There is no possibility of having more (or less) saving than investment, andwhile we might like to save more, we cannot do so unless investment is higher(so that income is higher, so that we can take that first step to savemore—then we take the second step regarding how to save). This is related tothe paradox of thrift (go here for more).

Carney has adopted the amusing (nay, hysterical) andconfused exposition over at MMR which rewrites the one sector model as:

0 = 0 so now add S to both sides

0 + S = 0 + S now add I to both sides and subtract 0 fromboth sides

I + S = I + S now subtract I from both sides

S = I – I + S now regroup

S = I + (S-I)

Here is what the MMR folks claim about it:

“Hence, our focus on S=I+(S-I) with the emphasison the idea that “the backbone of private sector equity is I, not Net FinancialAssets.” The idea is not novel, but simply clarifies the understanding of theprivate sector component.”

The equation isattributed to the “brilliant” analysis of some JKH—who is roundly praised byall those at MMR for coming up with the smoking gun against MMT and Godley’ssectoral balance approach.

This is the fundamental MMR equation that proves MMT wrong? Thething in parenthesis is excess or “net” saving. It is supposed to beeye-popping and revelatory, indeed, revolutionary in the deep meaning itexposes. It says that household saving is equal to investment plus the excess of saving overinvestment!

So a couple of hundred years of economics, let alone MMT’stwo decades of work, is completely overthrown: saving exceeds investment! By theamount that saving exceeds investment. But why stop there? Let’s introducegovernment.

G + S = G + I + (S-I) now subtract G from both sides:

S = G + I + (S-G-I)

Saving exceedsgovernment spending plus investment by the excess of saving over the sum ofgovernment spending and investment spending!

And let’s not stop there either: add infinity to both sides:

S + infinity = G + I +infinity + (S-G-I) now subtractinfinity and we get

S = G + I + infinity + (S-G-I-infinity)

So saving is bigger than government spending plus investmentplus infinity. And as we all know, infinity is a very big number. MMT is off byan order of infinity. My mind is blown, too. Since all the other variables arevanishingly small compared to infinity the equation actually says that savingexceeds infinity by the amount that saving exceeds infinity.

Take that plus four bucks to Starbucks and you’ve savedenough to buy a Latte.

Forty years ago “people” (purposely vague term, here, toprotect the not so innocent) had to take mind-altering chemicals to reach suchmind-boggling conclusions. For those who do not remember those episodes (eitherfrom imbibing excessively or from being too young to have been there during theTimothy Leary days) just watch the original Woodstockmovie and pay particular attention to the speeches by Arlo Guthrie and JohnSebastian.

Mind-blowing stuff.

Oh, and since we just celebrated the anniversary of what wasperhaps the greatest athletic performance of all time—Wilt Chamberlain’s 100point NBA game—I might mention that I’m taller than Wilt. By how much?, youask. By the excess of my height over his, of course.

Ok that was a bit of fun at their expense. I admit that Icannot figure out what they think they are demonstrating with the self-described“brilliant” equation.

So far as I can tell, all the MMR discussion then centersaround two claims. First, that it might be perfectly OK for the domesticprivate business sector to run deficits (net saving for it is negative) whilethe domestic private household sector runs surpluses, accumulating claims onthat business sector.

So far, so good. Not at all inconsistent with what I arguedon the MMP blog or in my 1998 book as demonstrated above. All are insidefinancial claims, and all net to zero. But lots of “real” activity could haveresulted—that raises productive capacity and so on. (MMRs then provide loads ofodes to entrepreneurial spirit and the like. Good. I’m down with them on that.)

Ok fine. But note that if the household sector continuallyran deficits against the business sector (even with the private sector inbalance) we could still get into trouble—and get a Minsky-type debt deflationsimply because households cannot service their debts to firms. And also note itdoes no good to go the other way: what if firms went increasingly into debtagainst the household sector? Yes, they could get into trouble if gross incomeflows were not enough to service debts.

But MMRers ignore that as they jump to the conclusion thatit is perfectly fine if the business sector’s deficit exceeds the householdsector’s surplus—so the private sector taken as a whole is running a deficit.

Now, that is impossible in the one sector model (I=S).They’ve pulled a rabbit out of a hat and slipped in a second sector. Say it isthe foreign sector. In that case, we’ve got a positive capital account (netexports are negative) and the proper equation is not the one they write, butrather S = I + (-NX), as net exports are negative, or S = I –NX. What thismeans is that foreigners are accumulating claims on the domestic privatesector. Or, the domestic private sector is getting deeper in debt—toforeigners.

Is that alwaysbad? Of course not. But if it happens year after year after year, should we beconcerned? Perhaps. We might not be able to service the ever-growing debt offirms. And they might claim some of our real output.

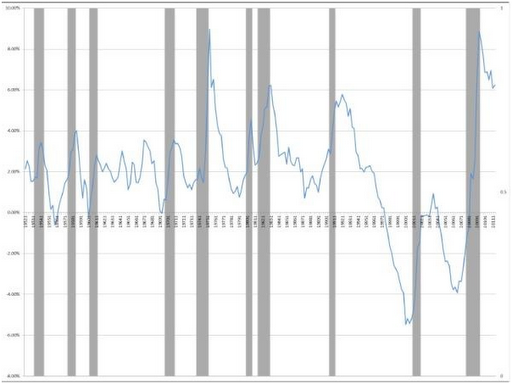

The other possibility is that the second sector isgovernment—with government accumulating claims on the private sector. Alwaysbad? Not necessarily. But when it continues trend-like, “history shows”–asGreenspan used to love to say–it is followed by a deep downturn (6 out of 7 timesin the US continued federal government budget surpluses were followed by adepression; the seventh by the GFC). And even if we just look at tighteningbudgets—not necessarily full-on budget surpluses—recessions almost alwaysfollow. In the following picture the blue line shows the private sectorbalance—and as its surplus (or net saving) declines we usually see a recession(shaded area) soon after. In other words, empirically it certainly does looklike reduction of net saving by the private sector is a pretty good indicatorof a coming downturn—so this is not normally a good thing after all.

Second claim. TheMMR people immediately moved on to “real saving” with some farmer whose cowsomehow morphs into 10 cows, with the extra 9 cows “saving” that resultswithout any deficits at all. (I take it that they don’t know much about animalhusbandry.) Anyway, let us pretend that a cow can give birth to 9–count ‘em,nine!–calves and has got enough teats to keep them alive.

What does that have to do with nominal saving and nominalinvestment and hence the equations we’ve been going through? Who the heckknows? I think we need some of those mind-altering chemicals or math equations toget our brains around the “brilliance” of the analysis.

OK. Real stuff, real production, real saving—we’ve switchedour definition of saving again. Theclaim is that MMR is more “real world” while MMT is somewhere out in the etherof theory land. Actually, I always allowed for “real saving”—as in a farmer whoplants his own seeds, harvests them and saves some for next year. But note thatone of the “Ms” in MMT (and presumably MMR) denotes “money” and hence focuseson the monetary system. That is not because we fail to recognize that there is“real stuff” and “real saving” but because we did not see any need to correct“Ricardian” economics that already deals with all that. Our complaint was thatmainstream economics has got money all wrong.

{Apparently the R in MMR stands for “realism”or some such adjective—as in cows with 9 teats is more “realistic” than thecows I grew up with that had a mere four—occasionally and exceptionally five orsix but that is no match for “modern money realism” that has cows with 9 teats (andpresumably several udders). Perhaps a bitof instruction for our MMR buddies about “the birds and the bees” might benecessary, because you see, cows don’t replicate without bulls—so even if yougot lucky and your cow had a male calf the first time around, to get more cows,that male would have to grow up and mate with his mom—which would lead to allof his buddies calling him an unkind word that begins with “M” and ends with“R”, and it is not “MMR” that they would call him. So aside from the ninecalves and nine teats we’ve got a bit of a problem explaining where the bullscame from to make the “real stuff” that is the subject of MMR economics.}

Are the MMTers confused on this? I had several sections inthe MMP to address the real junk. Let me see what I said, as Carney and theMMRs seem to have overlooked it.

Here is Blog 2’sdiscussion of real assets: A noteon nonfinancial wealth (real assets). One’s financial asset is necessarily offset by another’s financialliability. In the aggregate, net financial wealth must equal zero. However,real assets represent one’s wealth that is not offset by another’s liability,hence, at the aggregate level net wealth equals the value of real(nonfinancial) assets. To be clear, you might have purchased an automobile bygoing into debt. Your financial liability (your car loan) is offset by thefinancial asset held by the auto loan company. Since those net to zero, whatremains is the value of the real asset—the car. In most of the discussion thatfollows we will be concerned with financial assets and liabilities, but willkeep in the back of our minds that the value of real assets provides net wealthat both the individual level and at the aggregate level. Once we subtract allfinancial liabilities from total assets (real and financial) we are left withnonfinancial (real) assets, or aggregate net worth.

And, what do you know, there is an MMP with the title: Blog 17: Accounting for Real VersusFinancial (or Nominal). I wonder if it might have discussed the real junkMMR is concerned with? Let us see.

Blog 17: The state’s monetary unit isa handy measuring device that we use to measure credits, debts, and something fairlyesoteric we might call “value”. …We need a measuring unit that is appropriateto measuring heterogeneous things. We cannot use color, weight, length,density, and so on. For historical reasons I will not go into right now, weusually use the state’s money of account. Otherwise, we can only measure valuein terms of the thing itself. For example it is fairly easy to measure thevalue of sugar in terms of sugar—sugar weight will work, and if the crystalsare uniform we could actually count them out. Usually however we measure sugarby volume at least for kitchen purposes…. When I go to tally up all of mywealth I will include all the Dollar IOUs I hold against banks, the government,other financial institutions, friends and family and so on. That is my grossfinancial wealth…. Against that I count up all of my own IOUs—to banks,government, family and friends.

Now clearly I am notdone. I’ve got a house and a car… Assume I’ve got some debt against them, asI took out a loan (issued my own IOU to the bank or auto finance company, etc).That is part of my financial IOUs included in the calculation above. But I’vebeen paying for years and so the outstanding IOU is much less than the value ofmy car and home. I count the monetary value of the car and home and add that tomy financial assets to get gross assets. Now exactly how I value the house andcar is tricky and subject to accounting rules. But that is not important tounderstand the principle here. We take the total value of gross assets(financial plus real) and subtract the outstanding liabilities (usuallyfinancial, but there could be some real sugar IOUs) to get net wealth. That ofcourse, will be comprised of real assets plus net financial wealth. So totalnet wealth will be greater than net financial wealth because I’ve got realassets (car, house). (I could have negative net financial wealth thatis—hopefully—more than offset by positive real assets. Otherwise I am“underwater”.)

Most of the time in this primer we are focused on the monetary part of theeconomy—indeed on what Keynes called “monetary production” and Marx calledM-C-M’) in which production begins with money, to produce a commodity for salefor “more money” (profits). We focus on that because that is basically whatcapitalism is all about and we are mostly concerned with how “modern money”works in a capitalist economy. (Note, however, that “taxes drive money” appliesto earlier societies that were not capitalist.) Still even in capitalism it isobvious that not all production involves money in the beginning and not all isundertaken on the prospect of making profit. In about two hours I am going tofix dinner and wash dishes. I am not going to get paid, much less earn anyprofits. Now at least some of this “production” process does begin with money—Ibought most of the ingredients for the cooking, and purchased both water andsoap for washing. But part of the ingredients (especially my labor) will not bepurchased. Is this kind of production important? Undoubtedly—even in a highlydeveloped capitalist economy like the American it is hard to see how any of themonetary production could take place without all of the unpaid labor involvedin “reproducing” the “labor power” (these are Marx’s terms—you can replace themwith “supporting the family that supplies workers”). Domestic services, childrearing, recreation and relaxation, and so on are critical and mostly do notinvolve monetary transactions. We can—and sometimes do—put monetary values onthem anyway. Not only is there a “flow” dimension in the form of dailydishwashing, but there is also a “stock” dimension—accumulation of theknowledge and skills our youngsters will need later (often called “humancapital” by economists). That (growing) stock should be added to our “real assets”and hence to our total net wealth. Obviously, these things are very difficultto measure in Dollar terms.

So, does that make us remiss in not discussing “real”production and “real” accumulation? I cannot see how.

I could have put this in terms of 1 cow replicating into 10cows through virgin births with ample numbers of teats and adequateself-produced hay to support the whole lot without money intervening at all.Humans have overseen such miraculous multiplications (and even more than thisif you can count the Savior’s water into wine and bread into fish—if I’ve gotthe stories right for I must admit I slept through a lot of that instruction)for thousands of years before there even was a monetary economy. In otherwords, the nine teated cows that MMR trots out have nothing to do with moneywhatsoever, and hence the MM part of the MMR is not even called into play toexplain the miracles as “realistic” but not “modern money”. Truth in labelingshould truncate the MMR site to just “R” as its concern is not money, modern orotherwise. It is the “Real 9 Teated Cow and Immaculate Conception” theory ofeconomics, or R9TCIC website.

Theme Two: MMTignores corruption in government.

Carney: It’s a shame that a guy as brilliant as Wray doesn’t quiteunderstand that the “public sphere” is nearly always code for privateinterests expressed through political power.

OK, but JKH is also called “brilliant” so I’m not sure ifthat is meant as a compliment or a diss. Does Wray recognize that privateinterests are expressed through political power? Does Wray ignore what has beengoing on in Washington as the Bush-Clinton-Bush-Obama administrations turnednot only Washington but virtually our entire economy over to the banksters onWall Street? Has NEP totally overlooked problems of corruption?

There aren’t many economists (and certainly none of the MMRspseudo-economists) who’ve written more on the frauds perpetrated by Wall Streetand the “revolving door” operated by all of these administrations that haveessentially turned the Treasury as well as the White House staff over tofinancial interests. And this is not some new-found concern—I also wrote aboutfraud and the involvement of government officials during the S&L crisis.(Admission: I was far too skeptical of Bush, senior’s response—little did Iknow that a guy named Bill Black would play a major role in resolution of thatcrisis—helping to put 1000 crooks behind bars; compared to Clinton and Obama,Bush sr came out of that crisis looking relatively clean.).

And I do not know how Bill “Control Fraud” Black, one of themain contributors to NEP—who literally “wrote the book” on bank fraud, can becharacterized as someone who does not understand that political interests getexpressed through political power. Does Carney really believe we all havechecked skepticism at the door when we advocate a positive role for publicpolicy?

Truth be told, I’ve been disappointed and even horrified bymuch of the US federal government’s policy since the days of LBJ. I will admitto buying-in to JFK’s Camelot when I was a kid, and I can remember the exactinstant when the closest neighbor to my one-room school house burst into theclassroom to announce on the afternoon of November 22, 1963 that he had beenshot (we had no telephone, or even running water; and our textbooks weregloriously out-of-date so that we did not need to worry about WWII and postwardevelopments—there were only 48 states to remember, 7 known planets to study,and 31 president’s names—up to Hoover–to commit to memory). While most of theclass cheered (some of that was due to the following announcement that we’d begoing home, but most of it was due to the politics of the little Rick SantorumsI counted as school chums) my own world was shattered. My family was then “allthe way with LBJ” until he ramped up the war against Viet Nam—and from thatpoint on I was never confused about the influence of private interests over thepublic purpose. Come on, the next President was Tricky Dick, after all—whobrought the war home to attack our nation’s youth. And it was downhill afterthat. At the time, I never thought I’d look back on Tricky Dick as—arguably–themost progressive president of the past half century. Shame on those whofollowed him.

Theme Three: There isno public purpose.

Carney’s claim goes much further—he rejects the notion ofpublic purpose and asserts that government’s contribution to the economyapproaches zero.

Carney: I suspect thatmost government spending is socially destructive and economically malfeasant,and nearly all discretionary government spending is thoroughly corrupt, thisseems to bother them less. My “right size” of government is far smaller—almostvanishingly small—than theirs. (Here’s Randall Wray, on of the leading MMTacademics, arguing that government should spend 30 percent of GDP! Saints preserve us!)

Ok, sounding a lot like Rick Santorum, Carney invokesreligion to save us from those godless MMT Keynesians who advocate biggovernment. Now, in truth I never argued government “should spend” 30% of GDP.My whole article was arguing that it makes no sense at all to focus on suchratios. Instead, I asked all of us to put on the table what each of us believesto be worthwhile activities of government. My overriding point was that wecould have all of the progressive wetdream utopian programs and it would still amount to less than 30% of GDP.Hence, my whole argument was precisely the opposite of what Carney’s accusationproclaims—my summing up of expenditures was to demonstrate that we’d still beleft with a relatively small government, certainly in comparison to the size ofgovernment of all other developed capitalist countries—even if we adopted thefull progressive wish list. And my point was to lay-out what governmentactually spends for so that our Austrian friends could tell us exactly whichprograms would get cut.

Unfortunately, they respond only with handwaves—just likethe anti-government Republican candidates who refuse to tell us what they willcut, on the certain recognition that their views have almost no overlap withthe American public’s. Instead they argue for a “vanishing small” governmentwithout telling us what, if anything, they’d cut and what, if anything, they’dretain.

Carney: For the record I should say, I’m way more libertarian than theMMR guys. Maybe I’m Neo-MMR.

Again I want to be clear. Reasonable people candisagree—that was the main point of my “MMT for Austrians” piece. Libertarianswant a much smaller government. I have no problem with that. Go ahead, put yourextreme ideology on the table. List which programs you support and let us totalthem up. Tell what you are going to cut. Take the heat. You’ll be soundlyrejected by the 99% of the population that can figure out whose side you areon.

But Carney seems toargue much more than that. His claim comes close to arguing that there is norole at all for government.

Carney: What Brooks getsand Wray misses, however, is that government spending priorities areeconomically damaging. When resources are moved “to the publicsphere” they are utilized to realize political ends rather than”public” ends. That is, they are used to satisfy the demands ofspecial interests who influence lawmakers and regulators. This gap inunderstanding is one of the things that has given rise to the post-ModernMonetary Theory movement of Modern Monetary Realism.

As an ideological statement, I have no problem with this.Reasonable people can disagree. It is Carney’s belief that government reallycannot do anything positive. But he goes on, proclaiming this is fact, notideology:

Carney: This is notideology. These are conclusions from decades of investigating the waygovernment operates. As you guys like to say in other contexts, we’ve done thework so you don’t have to. Read my brother’s book.

So, according to Carney, decades of investigations revealthat “government spending priorities are economically damaging”.

In my post on NEP I had detailed exactly what governmentspending is, across the major programs. There really are only three main areasof spending that are large enough to make much difference to the overall budget:defense, Medicare, and Social Security. So if we are talking about “priorities”we must be talking about these areas. In my piece, I had advocated substantialdownsizing of the defense sector (which I do see as economically and politicallyand morally damaging)—so when Carney argues that I “miss” the fact thatspending priorities are “damaging” he must be referring to Medicare and SocialSecurity.

Does Carney really believe that crediting the bank accountof some 90 year old widow so that she can afford to live a more-or-lessdignified life on Social Security is “economically damaging”? What is theeconomic evidence for the claim? Does he mean incentives? Without SocialSecurity, she’d be incentivized and available to work—maybe at Burger King? Ordoes he prefer the third world model—she would be sitting on a blanket andselling “Chiclets”—pieces of gum—and dumpster diving for scraps of food? He’dproperly align the incentives by taking away her Social Security benefits?Please, Carney, tell us how Social Security benefits damage the economy andwhat you would put in their place.

What about the people with disabilities who also collectSocial Security? I used to live in Mexico and can recall the “safety net” forthe man with no legs who had to cross busy lanes of traffic each day to get to“his” spot where he begged for coins. That’s the “free market” solution todisabilities. Is this the future Carney sees for our citizens living withdisabilities?

Or is it Medicare—medical care for our aged—that is“economically damaging”? In what ways? And what would be the preferred and lesseconomically damaging alternative? Just ignore healthcare needs of the bottom99% that cannot afford care? If that 90 year old widow breaks a leg, you thinkit would be less economically damaging to just let her lay in bed and wasteaway, rather than putting her in a cast so she can serve burgers as she mends? Andif a program like Medicare is so damaging, why is it that health outcomes arebetter in almost all countries that have government-paid universal healthcare?And overall living standards are higher in most of them?

He goes on, apparently to soften the conclusion a tiny bit:

Carney: But because theseare conclusions drawn from years of investigation and research, I don’t thinkit’s terrible that you find them implausible…. although I draw pragmaticallylibertarian lessons from the facts about public policy production, there areother possible lessons that decent people could arrive at. Even if governmentspending is as bad as I say it is, it may be necessary to accomplish otherthings that are absolutely required. For instance, the defense industryis a racket. But if we were invaded or under threat of invasion, I’d put upwith letting the arms dealer loot us because that’s the only way to get enoughguns to defend the country.

I wonder if Carney would carry this a bit further. Let ussay for the sake of argument that every government project is subject tocorruption. Carney’s willing to trade off some corruption for defense of thenation. Would he draw a pragmatically libertarian lesson that it is stillbetter to have an interstate highway system in spite of the supposedinefficiencies of the “racket” of “looting” by road construction workers andfirms?

How about clean water? Working sewers for flushing toilets?Police force? Public schools and universities? Government support for R&Dthat resulted in the 747, computers, the internet, vaccinations that have wipedout most of the worst childhood diseases?

Would he take a bit of inefficiency and public corruption asa tradeoff to have security in those areas?

In short, all of those things that separate life in the USand all other developed countries from the low living standards in thedeveloping nations with the very small governments that Carney prefers? Orwould he rather forgo all of that because there is some corruption?

Has Carney overlooked all the advantages of a governmentthat recognizes and supports the notion of public purpose, in spite of all ofits flaws? Is Carney only willing to overlook the obvious flaws of—say—avirtually unregulated financial system that—arguably–has in just four shortyears resulted in greater economic losses than the sum total of all government“inefficiencies” of the past few centuries?

I have never been in any country, anywhere, in whichaudiences do not readily recount horror stories about government corruption. Ithink these stories are mostly true. And, yet, most places I visit havetolerably good public infrastructure and services, paid for by “corrupt”government always in “cahoots” with a thoroughly corrupt criminal class in theprivate sector.

Carney would point his finger at government and prefer todownsize it—while leaving provision of services and infrastructure to a greatdeal of luck and hope that kleptocratic private sector crooks will be guided byinvisible hands to operate in the public interest while making profits for theprivate interest.

Yet, for every Geithner shoveling public money to privatesector banks, there are a dozen Blankfeins subverting the public purpose. Yesthere is no doubt that there is a revolving door in every administration—all ofthe Clinton-Obama top dogs came from Wall Street and expect to go back withhigher incomes since they’ll funnel Uncle Sam’s money to their once and futureemployers. Isn’t it a bit strange that Carney’s response is to downsize orvirtually eliminate government, rather than going after the kleptocratic crooksthat undermine public policy?

I’d prefer to point my finger at the crooks in both theprivate and public sectors, and then jail them. I do not support eitherkleptocrats or invisible hand waves that suppose private interest, alone, isenough.

But Reasonable People can Disagree. Can’t they?

20 responses to “MMT FOR AUSTRIANS PART TWO: Disagreements Among Reasonable People”