Audio (mp3) of the FCIC’s interview of William Black are avialable in two parts on the FCIC’s website. Links to the mp3’s follow.

Audio (mp3) of the FCIC’s interview of William Black are avialable in two parts on the FCIC’s website. Links to the mp3’s follow.

I think terror ranks right up there with fraud and corruption, but let’s grant your point for the moment. Were you turning a blind eye to PLO corruption? Can you point to posts or articles you wrote in the PLO era? If not, I think these posts are more anti-Israel than anti-corruption.

Second, he asks “were you turning a blind eye to PLO corruption?” PLO corruption is irrelevant to the strategy that the JPost columnists were implicitly advocating of the U.S. bribing Egyptian generals in order to induce them to murder and maim Egyptian civilians. No one was implying that Israelis were uniquely corrupt. The corruption at issue was Egyptian corruption.

Third, Anonymous thinks my posts are “anti-Israel” unless I can produce multiple posts attacking PLO corruption. Putting aside the fact that the “PLO era” (if I understand how Anon. is using that phrase) ended before I began making posts a bit over two years ago, the writer misses a more fundamental point. None of my columns are about Israel — they are about particular JPost columnists. My columns are distinctly pro-Israel (without being anti-Muslim). I stress that Israel has, despite its military dominance, refused for moral and pragmatic reasons to employ “Hama Rules.” I stress that Israel has refused to attempt to bribe Egyptian generals to induce them to launch a wave of terror against their citizens for the purpose of keeping Mubarak in power. Anonymous makes the error of conflating specific JPost columnists with Israel. Again, I stress that Israel refused to follow their strategy suggestions – Israel returned the Sinai to the nation from which it was taken by force of arms – Egypt. Israel refused to employ the bribery/terror strategy. I believe that the policies the columnists have recommended would have been anti-Israel, anti-Egypt, and anti-U.S. I think President Carter’s successful shepherding of the Peace Accords was pro-Israel, pro-Egypt, and pro-U.S. I think that if President Obama had employed the bribery/terror strategy that the JPost columnists advocate it would have been anti-Israel, anti-Egypt, and anti-U.S.

While I did not blog until fairly recently, I did write a letter to the editor of Al-Ahram, Egypt’s leading English-language paper, nearly a decade ago. I’ve set out the full text below.

Words in Bin Laden’s mouthSir- Several of your opinion writers this week share the same flaw — the desire to claim that Bin Laden revels in the mass murder of innocents because of the cause that is dear to the writer’s (but not Bin Laden’s) heart. Thus, we are told that thousands were massacred on 11 September because of global income disparities, or because the US is arrogant, or because the US does not put enough pressure on Israel to make peace.In fact, none of those things motivated Bin Laden. Even his most recent video, which for the first time tries to highlight the Palestinians, makes that clear. Bin Laden has made it abundantly clear that what lit his fuse was the presence of “infidels” “defiling” “holy Arabia” (i.e., American troops risking their lives to defend his native country from imminent invasion by Saddam).Now, as I recall the position of Arab and Islamic states at Durban, any state that discriminated against others on the basis of their religion was “racist” and engaged in “apartheid.” I trust you will show some minimal consistency and agree that Saudi Arabia already does discriminate against other faiths (e.g., displaying a crucifix can be a crime) and that Bin Laden wants the total exclusion of “infidels.” The US should not accede to such bigotry, our soldiers do not “defile” a country by defending it, and it is a Wahabi/House of Saud “creation myth” to call all of Saudi Arabia “holy.” Moreover, in a desire to respect local sensibilities (even bigoted ones), US troops are kept hundreds of miles from Mecca and Medina. Further, the US did a very good thing in defeating Iraq, defending Saudi Arabia and liberating Kuwait. The world would be much worse off but for these US actions. Therefore, whatever policies we followed with regard to Israel, Bin Laden would still have wished to engage in the mass murder of Jewish and Christian civilians (“Crusaders” in his argot).The claim that Bin Laden massacred American civilians out of global poverty is absurd. He’s rich and his principal lieutenants, like Atta, were well-to-do. The US could increase foreign aid a hundred times over and he would still seek our blood.Nor can the US possibly, morally, accede to Bin Laden’s demands about Israel. He wants the restoration of the universal caliphate, the recovery of all lands ever ruled by Muslims, and the mass murder of those who stand in the way of this restoration — including women and children. We will not accede to the destruction of Israel or further terrorist attacks. No reputable American will. So, Bin Laden will still seek to murder us even if our efforts to aid the peace process succeed. You know full well that Bin Laden hates the peace process and wishes it to fail. You know full well that he planned these attacks at the very time that US carrots and sticks led to an Israeli offer for return of land that came very close to producing a final peace agreement.One of your opinion writers says the critical question Americans should ask is why 19 Arabs were willing to sacrifice their lives to massacre thousands of innocents. I’ll address that question, but I’ll start with a question of my own. What caused five or six unarmed Americans to be willing to give up their lives attacking four armed terrorists in order to save the lives of people they didn’t even know? I am talking, of course, about the hijacked plane that crashed in Philadelphia. It was love. What caused the terrorists to act as they did? It was hate.That hate was very carefully taught. The death of thousands has become a mere statistic to your opinion writers, so try this one instead: the terrorists took female flight attendants, bound their hands behind their backs, and slit their throats. As I write, thousands (not a handful) of Palestinians are rioting to show their support of these heroic murderers of defenceless American women. Arafat is repeating the strategy he used when many Palestinians celebrated the 11 September massacres, by seeking to suppress television reporting of the pro-Bin Laden riots in Gaza.If you are truly concerned about global poverty, consider the effects of Bin Laden’s massacres on the world economy and who will be the worst losers from the coming global recession — the poor. Consider also what oil shocks do to the poorest of the poor. Sub-Saharan Africa has never recovered from OPEC’s successful foray as a cartel. Saddam came very close to controlling Iraq, Iran’s primary oil-producing region, Kuwait and Saudi Arabia. Want to hazard a guess as to the oil shock he would have engineered and the impact on the (net oil importing) Third World?William K. BlackAssistant professorUniversity of Texas at AustinLBJ School of Public Affairs

(cross-posted with Benzinga.com)

The risks to Fannie and Freddie are governmental, not financial. The government could decide to do extremely destructive things to Fannie and Freddie.

The risks to a privatized Fannie and Freddie (by whatever name) are even greater. If the existing systemically dangerous institutions (SDIs) became private label securitizers they would have all the perverse risks that come from modern executive compensation. They would pose a systemic risk if they were to fail – which is why regardless of how much the government promised not to bail them out no one would believe it. That is why they would be GSEs regardless of their official designation. The more they are perceived as GSEs the greater the political risk that Congress will demand dangerous actions from the private label securitizers.

It is not clear why the administration believes that securitization of mortgages is necessary or even desirable. Portfolio home lenders will face prepayment and interest rate risk, but those risks are simply transferred, not removed, by securitization. Given what we have learned from the crisis, the assumption that securitization leads to an efficient distribution appears baseless. Some banks will doubtless fail if interest rates increase sharply and remain high for many months, but hedging and macroeconomic policy can greatly reduce the failure rate among banks.

The first step, however, should be to make the existing disaster that is Fannie and Freddie fully transparent. We need to investigate fully what went wrong. If Fannie and Freddie put all their information on the web we could bring the wisdom of the masses to bear and determine the truth. There is no reason why Fannie and Freddie should have broad proprietary secrets.

Posted in Policy and Reform, Uncategorized, William K. Black

Why? Does he think Netanyahu could have prevented Egyptian unrest? Did he provoke Egyptians in any way? Why would Israelis blame Netanyahu for something on which he had no control? I read Telhami’s column once and twice and couldn’t quite get it.

Who stabbed Germany in the back? Who sabotaged the German army when it was on the verge of victory? Who betrayed the Fatherland by giving the British our secrets so that their Navy could blockade our ports and starve our people? Who destroyed our economy and our currency? It was always the same group and you know who they were. Answer me now – who did all these things?

I understand and agree with Rosner’s criticism of Telhami’s prediction. It makes no sense to blame Bibi (Netanyahu’s popular nickname) for something “on which he had no control.” But the JPost is chock full of columns, including one by Rosner, that blame President Obama for Mubarak’s fall. Unlike Telhami’s column, which is respectful, the tone of the JPost columns attacking Obama is exceptionally strident. Why doesn’t Rosner recognize that it is absurd to blame either the bicyclists (Obama) or the Jews (Netanyahu) for Mubarak’s loss of power? Why not blame Mubarak and his cronies and family – who the Egyptians came to despise?

The efforts by JPost columnists to blame Obama for Mubarak’s fall are less coherent than Telhami’s critique of Netanyahu. Ms. Honig claims “Obama ushered in chaos even if he chose Cairo as his venue for the 2009 speech in which he sucked up to Islam [sic].” Obama gave a speech on June 4, 2009 that supposedly caused street revolts in Cairo 18 months later. In reality, the revolt in Tunisia sparked the protests in Cairo and the revolt in Tunisia was caused by the usual combination of corrupt, failed, and autocratic leadership plus a random event. As even Honig concedes, Mubarak could not remain in power in any event because “Mubarak is old and ill.” He also had no successor with legitimacy that Israel would find desirable. Honig projects magic powers onto Obama – a speech, in English, by an American produced a national movement in Egypt.

But Rosner asks the right question, though he fails to ask it of his JPost colleagues: how was Netanyahu or Obama supposed to “control” either the Egyptian military or the protestors? Rosner finds the answer to that question about Netanyahu so obvious that it is clear that he considers the question foolish. Netanyahu could not “control” either the Egyptian military or the protestors. Netanyahu had no magic button he could push that would give him such control. Rosner sees all this with clarity. But he and his colleagues cannot see that Obama had no magic button. No one seriously believes that Obama can give a speech and cause the residents of Cairo to start or to end a revolt. The only conceivable magic button is bribery of senior Egyptian generals.

There are three crippling problems with the hypothesized Obama magic bribery button. First, what is supposed to happen if the bribe succeeds? “Successful” bribery would require the Egyptian army to kill, torture, and imprison enough Egyptians to terrorize the protestors to the point that the protests ended and did not resume. Even if the bribe and the repression succeeded, how long would Mubarak live and what destabilizing forces would the campaign of terror against Egyptians unleash? Second, the bribe would likely fail and blow up in the face of the nation offering the bribe. Imagine Al Jazeera interviewing an Egyptian general explaining that a foreign government offered him a $200 million bribe in return for a promise to order the Egyptian army to attack the protestors. Third, if Obama has a magical bribery button that can create a “successful” Egyptian army war of terror against the Egyptian people – then Netanyahu does as well. Mossad can run a “false flag” bribery operation of an Egyptian general by representatives of a pseudo-Saudi prince. Indeed, since JPost columnists have long employed their most derisive and insulting prose to demonstrate that the American government is hopelessly incompetent in understanding and influencing Arab and Iranian officials, Mossad should be dramatically superior to our CIA in arranging such bribes and directing the resulting campaign of terror against the Egyptian people. If Obama “lost” Egypt by failing to bribe the Egyptian generals, then Netanyahu “lost” Egypt. (Indeed, every major nation with a intelligence service “lost” Egypt under this “logic.”)

Why didn’t Bibi order Mossad to bribe the Egyptian generals to order the army to attack Egyptian civilians? Because doing so would have been morally depraved, unsuccessful, and harmful to Israel. I am a white-collar criminologist. I study fraud and bribery by elites and have helped conduct investigations to detect it and systems to reduce it. Corruption is a severe problem in Egypt (and Israel), and corrupt senior leaders pose a risk to national security. But bribery has great limitations even in corrupt nations. A general who grows rich through kickbacks from defense contractors will typically refuse even huge bribes that would require him to murder fellow citizens who are peacefully demonstrating for change. It is easier to bribe the military to engage in terror when the nation is fighting a vicious civil war along ethnic divisions in which terror is the norm. That is not the situation in Egypt – and no Western nation understood that fact better than Israel. I predict that the Mossad did not present using bribery to instigate a wave of terror against the Egyptian protestors as an option to Netanyahu. I predict that the same is true of the CIA and Obama.

The CIA, contrary to JPost columnists’ typical derision, combined bribery, small units of special forces, and smart air strikes brilliantly in the initial campaign in Afghanistan in response to the 9/11 attacks. But the CIA also learned early in that campaign the limits of relying on bribery (and financial incentives such as rewards) to capture or kill the most senior Taliban and al-Qaeda leaders. Afghanistan also demonstrates the typical weakness of trying to create a reliable national government – seen by the population as legitimate – through bribery and the provision of ample opportunities for corrupt gain.

Mubarak lost Egypt – to the Egyptian people – who no longer feared or respected him or his children. None of us know what will come next. Mubarak’s successors could be far worse. Neither the U.S. nor Israel has a magic button to push that will determine his successors. There are great limits to U.S. and Israeli power and life is uncertain. That is the nature of the real world.

Comments Off on Rosner’s Portrayal of the U.S. Neo-Cons as Useful Idiots – Part 2

Posted in Uncategorized

Tagged Uncategorized

Efforts to attract and retain top managers at Freddie and its larger sibling, Fannie Mae, have been stymied by salary restrictions that are modest relative to comparable to private sector pay and by the fact that the firm’s federal overseers have effective veto rights over major decisions.

In 2007, then-Freddie Mac CEO Richard F. Syron had a base salary of $1.2 million and total compensation of $18.3 million, according to SEC filings. In the same year, Daniel Mudd, the chief executive of Fannie Mae, had a base salary of $987,000 and total compensation of $11.7 million.

I do not know why Witherell resigned. I hope he is not facing a family emergency. I write to ask why he was hired. Witherell’s principal experience was with Lehman. In particular, he was chief executive officer of Aurora Loan Services from 2003 to 2006. Lehman owned Aurora. Aurora specialized in purchasing and reselling “liar’s” loans.

I testified before the House Financial Services Committee on April 21, 2010 about Lehman and Aurora’s pervasive accounting fraud. A copy of that testimony can be found here.

The key point is that Aurora was a massive fraud — purchasing and selling often fraudulent mortgages. It is virtually certain that Freddie purchased material amounts of Aurora’s fraudulent mortgages (directly, or by purchasing collateralized debt obligations (CDOs) that were supposed to be backed by Aurora’s liar’s loans). As my colleague Randy Wray has emphasized, we need a new term for the toxic MBS (mortgage-backed securities) because they often weren’t backed by mortgages due to lender fraud.

The proverbial bottom line is that a global search for talent, after Fannie and Freddie’s second descent into accounting control fraud bankrupted both firms, Fannie and Freddie (with its regulators’ blessing, chose Witherell. (Heidrick & Struggles, which describes itself as the leading executive search firm, issued a press release praising itself for finding Witherell.) When Obama knew he had to clean up the Stygian Stables that were Fannie and Freddie — knew that their senior managers and their regulators had failed catastrophically — he left in charge the failed regulatory leadership team. The regulator team allowed Freddie to select as its COO one of the leaders in the creation of the liar’s loans that were the greatest single contributor to Freddie’s failure and the financial crisis. This was bizarre politics — the senior regulator Obama left in power until his voluntary resignation was a Republican chosen because he was George Bush’s close friend since their days together in prep school. It was even more insane regulatory policy.

Freddie (and Fannie) should be suing Aurora/Lehman for their frauds. Freddie and Fannie should be making thousands of criminal referrals against Aurora’s fraudulent loans. Witherell would be a key witness in the cases. Freddie placed him in impossible positions due to his conflicts of interest.

Aurora was notorious — why would anyone, much less Freddie, hire a top official from one of the firms most responsible for the frauds that destroyed Freddie and cost the taxpayers billions of dollars in losses? Is there anything that a business leader can do that disqualifies him from receiving millions of dollars annually — paid for by the taxpayers? It’s bad enough that our elites now loot with impunity. Do we really have to make them even richer?

Fannie and Freddie have no need to pay these high salaries to senior managers. It was the perverse executive compensation that drove the accounting control frauds at Fannie and Freddie — as the SEC explicitly charged. Executive compensation created the perverse managerial incentives that destroyed Fannie and Freddie. This was an unanticipated consequence of their privatization. Because Fannie and Freddie were privatized, their officers designed their compensation system in the same perverse manner as most firms (Bebchuk & Fried 2004). The mangers stood to gain enormous compensation if they inflated short-term accounting income, and as Akerlof & Romer famously observed, accounting fraud is a “sure thing.” Mr. Raines explained in response to a media question what was causing the repeated scandals at elite financial institutions:

We’ve had a terrible scandal on Wall Street. What is your view?Investment banking is a business that’s so denominated in dollars that the temptations are great, so you have to have very strong rules. My experience is where there is a one-to-one relation between if I do X, money will hit my pocket, you tend to see people doing X a lot. You’ve got to be very careful about that. Don’t just say: “If you hit this revenue number, your bonus is going to be this.” It sets up an incentive that’s overwhelming. You wave enough money in front of people, and good people will do bad things.

William Black was interviewed recently on the Real News regarding President Reagan’s role in the Savings and Loan Crisis. For video and complete transcript click here.

So where do American presidents fit in this dichotomy? Well, the supreme success from this Israeli perspective is — President Carter. The Camp David Peace Accords with Mubarak’s assassinated predecessor Anwar Sadat resulted in the peace treaty with Egypt that Mubarak honored. That peace, even if cold, gave Israel the critical strategic advantage of not having to defend against a major conventional attack from its South (more precisely, it reduced the risk of such an attack and provided time for the IDF to mobilize to halt such an attack). The Israeli opponents of the Camp David Peace Accords were the settlers — the group that now purportedly exemplifies “learn from experience” under Rosner’s dichotomy. The settlers, the leading “pragmatists” (as Rosner terms the Israeli opponents of Arab democracy) sought to block the Camp David Peace Accords that Rosner now concludes were the greatest boon to Israeli security.

Under Rosner’s dichotomy, the naïve philosophers obsessed with democracy were George Bush and the U.S. neocons who eagerly launched a voluntary war against Iraq based on lies. Rosner writes to emphasize “that there’s no such thing as an Israeli neocon. The Israeli establishment never believed in promoting democracy in the Arab world, and it still doesn’t. It never much cared about Arab democracy, period.” Rosner thinks that Americans do not understand Israelis; that we had the absurd belief that Israel cared about democracy. Americans have many weaknesses in understanding other nations, but Rosner has picked an area in which Americans largely got it right. As Rosner opines, even among U.S. neocons, the most deluded segment of Americans about the Mideast, “most of them do” know that Israelis do not favor democracy. Quite the opposite — democracy and demographics are Jewish Israelis’ greatest fears because they know that Israeli Jews and Arab Muslims and Christians despise and fear each other. Even Israeli Jews and Arabs have sharply negative views of each other. Jewish demographics push Israel steadily to the right and towards the ultra-religious.

As Rosner pictures the relationship, Israelis originally viewed the neocons and Bush as useful idiots. All the talk of democracy was pure foolishness, but Likud originally believed that having America invade Iraq and provide ever greater military support to the IDF would prove exceptionally useful. Israelis came to doubt how useful the neocons policies were when they observed (1) the voluntary invasion of Iraq made Iran dominant in the region, (2) the wars in Iraq and Afghanistan weakened the U.S. military and greatly reduced its power to credibly project power elsewhere in the Mideast, and (3) the neocons’ Arab democracy ideas led to Hamas taking control of Gaza in relatively democratic elections. The neocons proved to be un-useful idiots to Israel under Rosner’s dichotomy.

As any reader of the Jerusalem Post would find “completely predictable,” the villain of Rosner’s piece is not President Bush, but President Obama. President Obama is the villain because he is like President Carter. Rosner cites Binyamin Ben Eliezer’s attack on Obama as proof of Obama’s pro-democracy folly — because Obama is purportedly risking the peace treaty that Carter negotiated over the opposition of Israel’s leading “pragmatists” — the settlers. Neither Ben Eliezer nor Rosner feel the need to inform the reader that Carter negotiated the treaty that provided the great strategic advantage to Israel and over 35 years of peace between Israel and Egypt.

[Mubarak] is now in danger of being toppled with the prodding and blessing of President Barack Obama and Secretary of State Hillary Clinton.So, Israelis were stunned to wake up and discover that their American friend had abandoned Mubarak in favor of change. “The Americans brought disaster to the Middle East by calling for [Egyptian President Hosni] Mubarak to leave his country,” said Knesset Member Binyamin Ben Eliezer, a former defense minister and one of Israel’s most establishment-minded politicians. Right and left, coalition and opposition, all but a very few thought poorly of U.S. policy. Everyone felt that the Obama administration had once again been “naive,” or “hasty,” that it didn’t understand the region and didn’t understand the Arab mentality. Israelis were stunned–and somewhat frightened. After all, if Washington has dumped Mubarak, maybe peaceful Egypt is gone for good. And if the United States could desert such a valued strategic ally, maybe we’re next in line for the boot?

Of course, such fears are nonsense. Israel isn’t Egypt, and its ties with the United States run much stronger and deeper. It will not be abandoned with such haste, and anyway, why would anyone want to abandon Israel? Still, there’s something to these fears, because the Egyptian unrest emphasizes the extent to which American and Israeli interests in the Middle East can be different. The United States, for all its many faults, is a dreamer; and Israel is a cynical pragmatist.

Once the Shah lost control of “his” nation the U.S. goals included arranging safe exile for the Shah (which the U.S. did at some substantial cost, including the seizure of our Embassy and staff). U.S. solicitude for the Shah was an act of pragmatism — we were showing our autocratic allies that even if they lost control and were in danger of being executed the U.S. would be willing to safeguard them and their families even when that would enrage the new government.

It is fantasy, not pragmatism, to believe that Carter had some magic button he could have pressed that would have kept the Shah in power. What was Carter supposed to do? Instruct SAVAK to launch a dirty war of torturing, disappearing, and murdering the Shah’s political opponents? Instruct Iran’s military to turn automatic weapons on the crowds? Assassinate Khomeini? Fly in the ready brigade of the AirCav? To do what? The Shah was a weak, dying, and hated man. Any of these options were almost certain to fail, they would make us hated with a passion, and they would betray everything that makes America a great nation. Does Israel want the U.S. to adopt Assad’s “Hama rules”? (When Haffez al-Assad was faced with revolt in Hama, Syria’s fourth largest city, in 1982, he responded by destroying much of the city and murdering thousands of “his” citizens. The terror “worked” — the revolt was crushed.)

Israel has, for 37 years, had the ability to follow Hama rules because of its decisive military power. It has refused to do so for moral and pragmatic reasons. It should not criticize the U.S. for refusing to descend to a depth of depravity and anti-pragmatic stupidity that Israel wisely refuses to plumb.

The conventional wisdom in Israel about the situation in Egypt today, and the U.S. response to it is fantasy posing as pragmatism. Under the Israeli rewrite of history, the U.S. was eager to push democracy in Egypt and too naïve to understand that the Muslim Brotherhood would come to power and destroy the Camp David Peace Accords with Israel. In the real world, the Obama administration consistently emphasized its support for President Mubarak and refused to criticize him for his consistent denial of democratic rights to the Egyptian people. When the mass protests began recently in Egypt, Obama and Secretary of State Clinton responded by emphasizing their support for him and cautioning against the protests.

What changed the U.S. policy response was that it became clear that Mubarak had lost control of Egypt. The U.S. had no good choices from either the U.S. or the Israeli perspective. Pragmatism means recognizing the limits of one’s power and options and not assuming that there is some “silver bullet” solution that makes difficulties disappear.

The U.S. did not urge Mubarak to conduct a peaceful transition of power until it was clear that he had lost control of Egypt. Rosner’s language choices are all slanted to make Obama the villain. Consider the sentence he uses to begin the critical discussion.

[Mubarak] is now in danger of being toppled with the prodding and blessing of President Barack Obama and Secretary of State Hillary Clinton.

The U.S. was pragmatic, not naïve, in deciding that it could not keep Mubarak in power. Obama’s dominant policy goal was to attempt to influence the transition in order to maximize the chances that the successor government would continue to honor the Camp David Peace Accords with Israel. No good deed goes unpunished.

Consider also Rosner’s subtle slanting of this passage.

[I]f Washington has dumped Mubarak, maybe peaceful Egypt is gone for good. And if the United States could desert such a valued strategic ally, maybe we’re next in line for the boot?

The U.S. remains Egypt’s closest ally. That alliance is not hostile to Israel, indeed, it was essential to attain Egypt’s willingness to enter into the peace accords with Israel — which Rosner and Ben Eliezer agree is the most favorable event for Israel in over 30 years. U.S. taxpayers have provided tens of billions of dollars in aid to Egypt and Israel as part of our broader agreements to support the Camp David accords. Even in the Great Recession the American people have continued this aid without complaint.

The Egyptian people “dumped Mubarak.” If, and only if, Mubarak’s successor repudiates the Camp David Peace Accords, the U.S. will cease its aid to Egypt. Rosner is even more disingenuous in his claims that Israelis are worried that because we have not urged Mubarak to respond to the protestors with terror, Israel may be “next in line for the boot.”

Rosner then adds this bit of faux reassurance to Israelis.

Of course, such fears are nonsense. Israel isn’t Egypt, and its ties with the United States run much stronger and deeper. It will not be abandoned with such haste, and anyway, why would anyone want to abandon Israel? Still, there’s something to these fears….

Deregulation or lax regulation. Explanations that rely on lack of regulation or deregulation as a cause of the financial crisis are also deficient. First, no significant deregulation of financial institutions occurred in the last 30 years [p. 445].Moreover, the Federal Deposit Insurance Corporation Improvement Act of 1991 (FDICIA) substantially increased the regulation of banks and savings and loan institutions (S&Ls) after the S&L debacle in the late 1980s and early 1990s, and it is noteworthy that FDICIA—the most stringent bank regulation since the adoption of deposit insurance—failed to prevent the financial crisis [p. 446].The shadow banking business. The large investment banks—Bear, Lehman, Merrill, Goldman Sachs and Morgan Stanley—all encountered difficulty in the financial crisis, and the Commission majority’s report lays much of the blame for this at the door of the Securities and Exchange Commission (SEC) for failing adequately to supervise them. It is true that the SEC’s supervisory process was weak, but many banks and S&Ls—stringently regulated under FDICIA—also failed. This casts doubt on the claim that if investment banks had been regulated like commercial banks—or had been able to offer insured deposits like commercial banks—they would not have encountered financial difficulties [p. 446].

I will also not discuss in detail the enormous desupervision that occurred at the SEC that permitted the Enron-era frauds. The budget and staffing of the SEC were kept relatively flat while its workload grew enormously. The percentage of fillings it reviewed declined to five percent. Congressional Republicans consistently sought to cut the SEC’s budget and staffing levels in the 1990s. Criminologists refer to the result as a “systems capacity” problem. (see here and here)

As SEC enforcement director Robert Khuzami emphasizes, the SEC must serve as the regulatory “cops on the beat.” The staff and budgetary limits rendered the SEC incapable of performing its primary statutory mission.

In sum, Wallison’s history excludes the deregulation and desupervision that permitted the two massive financial crises that preceded the current crisis. We will see that Wallison also ignores the major acts of deregulation, desupervison and de facto decriminalization that made possible the current crisis.

Deregulation

This column addresses the role of deregulation in allowing the current crisis. I break the discussion in to three subsets: deregulation by legislation, deregulation by rule changes, and an odd hybrid – the SEC’s Consolidated Supervised Entities (CSE) program.

Deregulation by Legislation

Gramm-Leach-Bliley (1989) repeals the Glass-Steagall Act and Reduces CRA Examination

The repeal of Glass-Steagall demonstrates the complexity of what deregulation can mean. The banking regulatory agencies were extremely hostile to the Glass-Steagall Act. They eviscerated the Act by adopting rules and interpretations that created so many exceptions to Act’s separation of “banking and commerce” that the separation was rendered ineffective. The federal regulators also did not enforce the remaining provisions of the Act vigorously even before it was repealed in 1999. The combination of deregulation and desupervision by the banking regulators so gutted the Act that its formal repeal by the Gramm-Leach-Bliley Act in 1999 had little practical effect.

Wallison refers to a modest regulatory strengthening of the CRA rules in 1995, but he does not inform the reader that the GLB Act reduced the frequency of examinations of smaller and rural banks under the Community Reinvestment Act (CRA) and sought to discourage alleged extortion by housing activist organizations (e.g., ACORN) by requiring the disclosure of any agreements they made with banks not to challenge mergers. Senators Dodd and Schumer led the group of Democrats that successfully pushed these anti-CRA provisions on a reluctant White House because the Democrats were so eager to repeal Glass-Steagall. (see here)

Wallison does not disclose this deregulatory aspect of the GLB Act because it falsified his claim that the CRA caused the crisis.

If there is doubt that these lessons are important, consider the ongoing efforts to amend the Community Reinvestment Act of 1977 (CRA). Late in the last session of the 111th Congress, a group of Democratic congress members introduced HR 6334. This bill, which was lauded by House Financial Services Committee Chairman Barney Frank as his “top priority” in the lame duck session of that Congress, would have extended the CRA to all “U.S. nonbank financial companies,” and thus would apply, to even more of the national economy, the same government social policy mandates responsible for the mortgage meltdown and the financial crisis [p. 443].

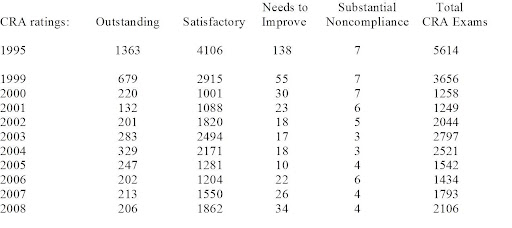

I prepared the chart below by searching the FFIEC data base for CRA rating by date of the CRA examination.(see FFIEC website here)

The chart confirms a number of points that anyone who has ever been a financial regulator after the passage of the CRA in1977 knows. CRA ratings have long been like Lake Woebegon’s children: they’re virtually all above average. Fewer than ten banks get rated as a serious problem – and even they get treated with kid gloves. Examine the data for 1999 and 2000. The examiners discover seven serious CRA problems in 1999 – slightly above one-tenth of one percent of the banks examined. That CRA rating “substantial noncompliance” triggered a requirement for annual CRA reexaminations of the non-magnificent seven and should have led to immediate enforcement actions. Clinton was President and had appointed each of the regulatory leaders. By 2000 the regulators appointed by Clinton (who Wallison seeks repeatedly to cast as the villains) acted so aggressively against the seven that the 2000 exams revealed that there were still seven awful banks. It’s not like banks were failing frequently in this period and requiring the regulators’ attention to be paid solely to “safety and soundness.” The claim that banks lived in fear of the CRA and that the CRA drove their lending decisions is pure fiction. Banks routinely got satisfactory or outstanding ratings by making good loans. Banks had to try hard to get poor ratings and even the tiny minority that did so rarely faced any meaningful sanction.

The data in the chart also show that the statutory deregulation, reducing CRA examination frequency, was significant. The number of annual CRA examinations in the 2000s was typically well under one-half of the number of CRA examinations in 1995. Wallison is deliberately disingenuous in stopping his discussion of CRA changes in 1995. Both statutory and regulatory deregulation of the CRA occurred after that date. (My next column will also discuss the desupervision of CRA compliance that occurred during the 2000s.) The CRA, and its enforcement, became weaker as the mortgage fraud epidemic surged. That (further) falsifies Wallison’s claims that the CRA was “responsible for the … crisis.”

Statutory changes that allowed the creation of “private label” MBS

The SEC, Department of the Treasury, and OFHEO (which regulated Fannie and Freddie) created a joint task force, which issued: A Staff Report of the Task Force on Mortgage-Backed Securities Disclosure in January 2003.

The Task Force report explained two key statutory changes that made possible the rise of private label

A number of regulatory and tax constraints initially impeded private entities from expanding into the MBS market created by the GSEs and Ginnie Mae.1. Secondary Mortgage Market Enhancement Act of 1984Many of the regulatory constraints affecting private entities were removed in 1984 with the passage of the Secondary Mortgage Market Enhancement Act of 1984 (“SMMEA”). SMMEA was intended to encourage private sector participation in the secondary mortgage market by, among other things, relaxing certain regulatory burdens that affected the ability of private-label issuers to sell their MBS.14 For example, SMMEA allowed state and federally regulated financial institutions to invest in privately issued mortgage related securities.2. Effect of Tax Laws on MBS MarketsTax law constraints also affected the types of MBS that could be sold. Until the passage of the Tax Reform Act of 1986 (“1986 Tax Act”), which recognized the Real Estate Mortgage Investment Conduit (“REMIC”) structure with its beneficial tax treatment, most MBS were sold as “pass-through” securities. As discussed below, pass-through securities pay an investor principal and interest received from payments on the mortgage loans that are the assets of the trust. The payments on the mortgage loans are passed through the trust to the investors as they are made.Before 1986, the effect of the limitation on activity of grantor trusts under the tax laws restricted the use of trusts with multiple classes of securities with differing payment characteristics. In the multi-class structure, the principal and interest payments are not just passed through pro rata as paid to all investors, but rather are divided into varying payment streams to create classes with different expected maturities, different levels of seniority or subordination or other differing characteristics. Prior to 1986, the tax law treated these multi-class trusts as associations taxable as corporations, and distributions would have been taxable at the trust level and also at the trust investor level. This “double taxation” made multi-class structures generally unfeasible.The 1986 Tax Act eliminated the double taxation for multi-class vehicles structured as REMICs. With the advent of the REMIC, more complex structures with multiple classes were developed which divided up the payment streams on the mortgage loans that were collateral for the securities repayment obligations to investors.

As late as October 2006, the view from the mortgage industry was that the private label MBS issuers were dominant and likely to remain dominant over Fannie and Freddie precisely because the private label issuers were far more aggressive than Fannie and Freddie in making far riskier loans to less wealthy Americans. Here’s how the Mortgage Bankers Association’s (MBA) trade magazine explained the role of Fannie and Freddie vis-a-vis Fannie and Freddie.

The rise of private label: innovative mortgage products, enthusiastic investor support and consumer demand for new affordable loans have all come together to give extraordinary new power to the private mortgage-backed securities market. This has left the private sector setting the rules once largely dictated by Fannie Mae, Freddie Mac and FHA.A change in the mortgage-backed securities (MBS) market that began more than two years ago appears to have completely reshuffled the industry’s deck of cards. Now, issuers of private-label residential MBS are holding the aces that were once held by the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac. Once a junior–but powerful–player in the market, private-label residential mortgage-backed securities (RMBS) are now the leading force driving product innovation and the net overall volume of mortgage origination. Further, it appears that the new dominant role for private-label RMBS may be here to stay.Product innovation has resulted from two developments, the first is mortgage consumers looking for new low-payment mortgages to help them afford rising home prices. The other is the growing willingness of investors to fund the new types of mortgage products that lenders have developed to meet this need.Mortgages that offer low monthly payment options often do not amortize the principal balance on the loan, and may even negatively amortize. These products–interest-only (IO) mortgages and option adjustable-rate mortgages (option ARMs)–are the primary generators of gains in market share for private-label issuers.There are also new nontraditional mortgage products that amortize, but extend the amortization term from the current 30 years to 40 and even 50 years in an effort to bring down the monthly payment.

The expectation that private-label issuers are likely to retain their dominant position was the consensus view of the [MBA’s] Council to Shape Change, a blue-ribbon mortgage industry panel of 19 experts that published its findings in August.The council, echoing what other market observers have said, cited the lag in product innovation as “the most important factor” holding the agencies back. “Most of the business now considered alt-A used to be prime business and would have fallen in the GSEs’ sweet spot,” the report states.Another factor in the market shift has been the ability of mortgage originators to increasingly securitize their own production. With this new capability, originators have been able to “adversely select the GSEs, feeding only product that lenders cannot advantageously securitize themselves,” the council’s report notes.Also, due to sharply rising home prices and the limits on the size of loans they can purchase, Fannie Mae and Freddie Mac are a minimal presence in states such as California, the nation’s largest mortgage market.To get a sense of the dramatic nature of the shift in market share, a few numbers help tell the story. As recently as 2003, the agencies issued 76 percent or $2.13 trillion of the year’s $2.72 trillion in mortgage-backed securities, according to data compiled by Inside Mortgage Finance (see Figure 1). These numbers include Fannie Mae, Freddie Mac and Ginnie Mae securitizations.In 2003, the non-agency or private-label RMBS was only 24 percent or $586 billion. Most of these were jumbo prime mortgages. The ground began to shift in the second half of 2004 as the refi boom subsided and interest rates began to rise, and home-price appreciation raced ahead at double-digit rates–prompting the introduction of a flurry of new affordability products.By year-end 2004, agency RMBS issuance represented $1.02 trillion, while the non-agency piece had risen to $864 billion out of a total of $1.88 trillion, according to Inside Mortgage Finance (see Figure 2).In 2005, the private-label RMBS surged into the dominant position, with $1.19 trillion or 55 percent of the $2.16 trillion in securities issued, while the agencies issued $966 billion (see Figure 3).

Note the comprehensive refutation of Wallison’s thesis provided by the findings of the MBA study. The MBA was an opponent of Fannie and Freddie because it believed that they acted to reduce yields on home loans. The MBA was overjoyed that Fannie and Freddie were losing market share. The MBA attributed Fannie and Freddie’s loss of market dominance to the private label issuers’ far greater willingness to make extreme risk loans to less wealthy Americans. The MBA explained that it was investors’ growing willingness to purchase toxic MBS issued by private label firms that was driving the rapid growth of the private label firms. The MBA study did not find that Fannie and Freddie were the investors purchasing the private label issuers’ toxic MBS. Douglas Holtz-Eakin, later appointed by the Republican Congressional leadership as an FCIC Commissioner, was one of the consultants to the MBA’s Council to Shape Change.

Wallison ignores the passage of the Commodities Futures Modernization Act of 2000

The Commodities Futures Modernization Act of 2000 created two regulatory black holes. Enron exploited one to help create the California energy crisis of 2001. The Act also created a massive regulatory black hole with regard to credit default swaps (CDS). Wallison does not mention the passage of the CFMA. He concedes that AIG took crippling losses from its CDS exposure but dismisses it as an “outlier” (p. 447).

Deregulation by Rule

Wallison fails to mention the major acts of deregulation by rule or interpretation that made substantial contributions to the crisis. I discuss four examples of this form of deregulation.

Rules Reducing Underwriting and Recordkeeping Requirements

On December 31, 1992, the Office of Thrift Supervision (OTS), and its sister federal banking agencies, adopted the Real Estate Lending Standards Rule (RELS), 12 CFR § 560.100-101. The OTS’ prior standard required minimum underwriting demonstrating that the borrower could repay the loan and that the collateral value was adequate to repay the loan in the event that the borrower did not pay. The OTS’ rule was of tremendous value in allowing the OTS to take effective supervisory and enforcement actions and the Justice Department’s fraud prosecutions. The OTS rules also required contemporaneous documentation of that the borrower had conducted the required underwriting. The joint agency standards, however, allowed the lender to establish its underwriting standards and its documentation standards. The result was a very substantial deregulation and impaired ability to supervise, take enforcement actions, and prosecute frauds.

Basel II Reduces Capital Requirements

Wallison mentions the Basel II deregulation only once in passing, without seeming to realize that it refutes his claim that there was no important deregulation in 30 years.

Beginning in 2002, for example, the Basel regulations provided that mortgages held in the form of MBS—presumably because of their superior liquidity compared to whole mortgages—required a bank to hold only 1.6 percent risk-based capital, while whole mortgages required risk-based capital backing of four percent [p. 476].

Rules and Interpretations Preempting State Laws and Rules

Wallison ignores deregulation via preemption even though it was a major aspect of deregulation in the current crisis. It is particularly understandable that Wallison does not acknowledge preemption because he favored federal regulators’ preemption of state efforts against predatory lending in his capacity as a member of the anti-regulatory and self-selected “Shadow Financial Regulatory Committee.” Statement No. 195 of the Shadow Financial Regulatory Committee on Predatory Lending and Federal Preemption of State Laws (September 22, 2003); Statement No. 186 of the Shadow Financial Regulatory Committee on State and Federal Securities Market Regulation (calling for federal preemption of then NY Attorney General Spitzer’s actions against securities firms) (February 24, 2003).

The federal agencies actually competed to be the most aggressive preemptors. The competition in laxity added greatly to the desupervision that will be the subject of my next column, but it also produced deregulation at the state level. The Commission report makes this plain.

The Comptroller of the Currency took the same line [as the OTS] on the national banks that it regulated, offering preemption as an inducement to use a national bank charter. In a speech, before the final OCC rules were passed, Comptroller John D. Hawke Jr. pointed to “national banks’ immunity from many state laws” as “a significant benefit of the national charter—a benefit that the OCC has fought hard over the years to preserve.” In an interview that year, Hawke explained that the potential loss of regulatory market share for the OCC “was a matter of concern” [p. 112].

Rules Further Reducing the Scope of the CRA

In addition to the statutory deregulation of CRA provisions wrought by adoption of the Gramm-Leach-Bliley Act in 1999, the federal regulatory agencies further reduced enforcement of the CRA by rule in 2004 and 2005 by expanding the definition of small banks from $250 million in assets to those with assets up to $1 billion. The rule changes reduced substantially the amount of information on loans the banks now considered small would have to provide and make public and reduced CRA examination frequency for many banks.

A Hybrid: the SEC’s Consolidated Supervised Entity (CSE) Program

There are regulatory actions that do not fall neatly into any category. The SEC, for example, created a regulatory structure for the purpose of blocking regulation. The context was that the European Union (EU) issued its Financial Conglomerates Directive was going to regulate the largest U.S. investment banks – unless they were regulated by the U.S. on a “consolidated supervision” basis. The SEC rushed to create a regulatory structure that the investment banks could voluntarily opt into – the Consolidated Supervised Entities (CSEs). The SEC’s CSE program was a sham. The SEC was supposed to act in an unprecedented capacity as a safety and soundness regulator (in addition to its role as a regulator of disclosures) over five of the largest, most complex financial institutions in the world. The SEC had no expertise and no systems that would allow it to succeed. But the Sec didn’t even try, its CSE program was a sham designed to block EU regulation of the largest investment banks. Each of the largest U.S. investment banks promptly volunteered to be regulated by the SEC’s CSE program. (The OTS, the weakest of the weak banking regulators, entered the competition in laxity with the SEC – and lost decisively. Each of the large investment banks voluntarily joined the CSE program. When an agency makes it clear that it will be a clearly weaker regulator than the OTS during the 2000s one knows that the agency has attained the status of flagrantly farcical.) The CSE program was so understaffed that it had three employees assigned to supervising Lehman. The CSE program was faux regulation. It created a de facto regulatory black hole for the largest investment banks that effectively reduced the investment banks’ capital requirements. The Commission report discusses the CSE program (pp. 150-155), the Republican dissents do not.

Conclusion

The three “des” – deregulation, desupervision and de facto decriminalization are the defining regulatory characteristics that, along with the perverse incentives of modern executive compensation and the ability of accounting control frauds to suborn purported “controls” (credit rating agencies, auditors, and appraisers) created the criminogenic environment that produced the epidemics of fraud that drove the current crisis. Wallison is correct that federal banking regulation law was made tougher in 1989 and 1991. On the SEC front, Sarbanes-Oxley attempted to toughen the securities laws. Each of those attempted positive statutory actions was overwhelmed by the rampant desupervision. Wallison is incorrect in claiming that there has been no significant financial deregulation in the last 30 years. There has been very little desirable financial deregulation in the last 30 years, but there has been extensive, destructive deregulation. Deregulation played a major role in the S&L debacle and the current crisis.

Click images to view details