By L. Randall Wray

In recent days MMT has captured the attention of anyone who can fog a mirror—even those long thought dead. The critics are out in full force—from the crazy right to the insular left. A short list includes Doug Henwood, Jerry Epstein, Josh Mason, Paul Krugman, Larry Summers, Ken “Mr Spreadsheet” Rogoff, Bill Gates, Larry Fink, George Selgin, Noah Smith, and Fed Chairman Powell. After laboring for a quarter century in the wilderness, the developers of MMT are pilloried for unleashing a theory that is “crazy”, “disastrous”, “hyperinflationary”, “nonsense”, “garbage” and just plain “wrong”.[1] Summers here; Rogoff here; Powell here; Krugman here; and here for Kelton Response

What all the critics have in common is that they have not bothered to read the MMT literature. Oh, it is just too much effort for the lazy critics! So they imagine what it must say, conjuring up the most ridiculous thing they can imagine, and then tear apart ideas so stupid that no one could possibly hold them.

And here’s the hilarious thing: every time we try to correct them, they say we are changing our arguments. Or, even funnier, they claim they’ve always held the crazy ideas and so we are saying nothing new.

So their critique goes something like this:

MMT claims that the earth is flat, and that the sun goes ‘round the earth. The first claim is false and everyone already knows the second. Heck, I’ve been arguing for two decades that the sun goes ‘round the earth. To prove it, I sat in my lawn chair last summer and saw the sun come up on the left, travel across the sky, and set on the right. It was hot but I persevered in the name of science. Most of what MMT says is false, and what it says that’s true is not new.

No folks. What you claim to be MMT is not MMT; what you claim you’ve always known to be true is neither MMT nor true.

I already offered a response to Doug Henwood’s here embarrassing critique (I notice that even most of his followers chastised him for his attack); Bill Mitchell responded to Professor Epstein’s neoliberal-like rant against MMT here (I might have more to say about it later); Stephanie Kelton has done yeowoman’s work battling the slippery Paul Kruman (demonstrating that he’s not only got MMT wrong, but his prognostications on the way the world works have been consistently wrong, to boot here); and I have a response to mainstreamers Paul Krugman, Larry Summers, Ken Rogoff (hey, Ken, have you figured out what a credit default swap is, yet?), and Chairman Powell in The Hill.

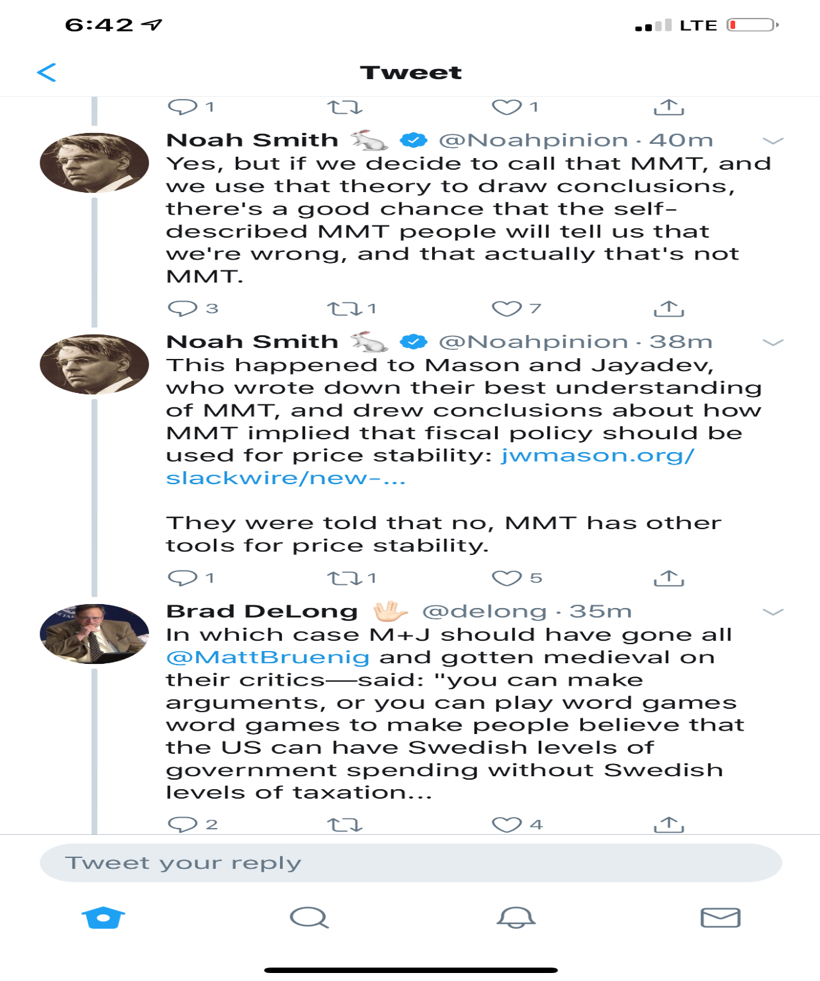

Here I want to respond to a challenge made by Brad DeLong (at the instigation of Noah Smith who garners undeserved attention for cribbing simplistic ideas from intro economics textbooks and passing them along as wisdom). Brad has often weighed-in quite reasonably on issues surrounding MMT so I’ll take his challenge seriously. I do not twit or tweet but these two twits were sent to me and will provide the background to his challenge.

Here’s the second.

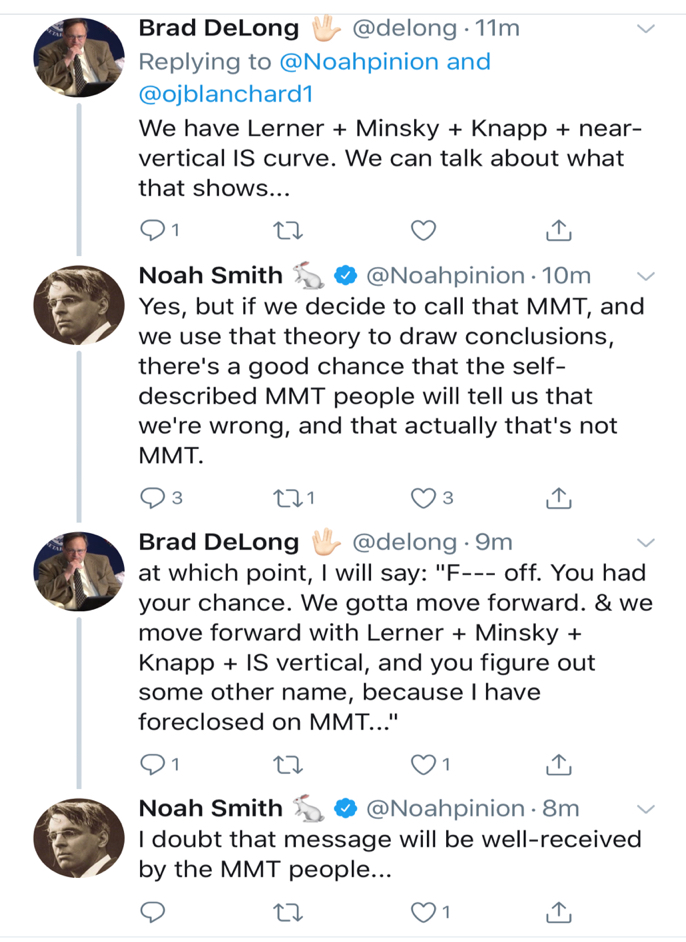

To summarize, we have Noah Smith complaining: if we decide to call something MMT, they will just tell us it is not MMT. Poor (Josh) Mason and Jayadev “wrote … about how MMT implied that fiscal policy should be used for price stability. They were told that no, MMT has other tools for price stability.”

Brad DeLong responds: “In which case M&J…should have gone all medieval on their critics—said ‘you can make your arguments or you can play word games to make people believe that the US can have Swedish levels of government spending without Swedish levels of taxes”.

I’m currently writing a longer piece with Yeva Nersisyan on costing and “paying for” the Green New Deal, so I’m not taking up Brad’s argument that we need “Swedish levels of taxes” here. (Hint: We do not need higher taxes to pay for “Swedish levels of spending”—but we do need high taxes on the rich to reduce their power.)

What I’ll focus on here is Mason and Jayadev’s “best understanding” and Brad’s challenge to accept or deny his characterization of MMT as Knapp+Lerner+Minsky+Vertical IS curve.

First, a bit more background. I was on the EEA panel with Mason where he presented his “best understanding” of MMT. He claimed that MMT is not a “settled body of thought” and decided that he can treat its components separately. He then proceeded to reduce MMT to the old Bastard Keynesian “pump priming” version of Functional Finance: just use fiscal policy to pump up aggregate demand until you get to full employment. He then criticized us for supposedly believing that then you’d need to pass tax hikes to fight the inflation set off by full employment. That’s supposed to be MMT.

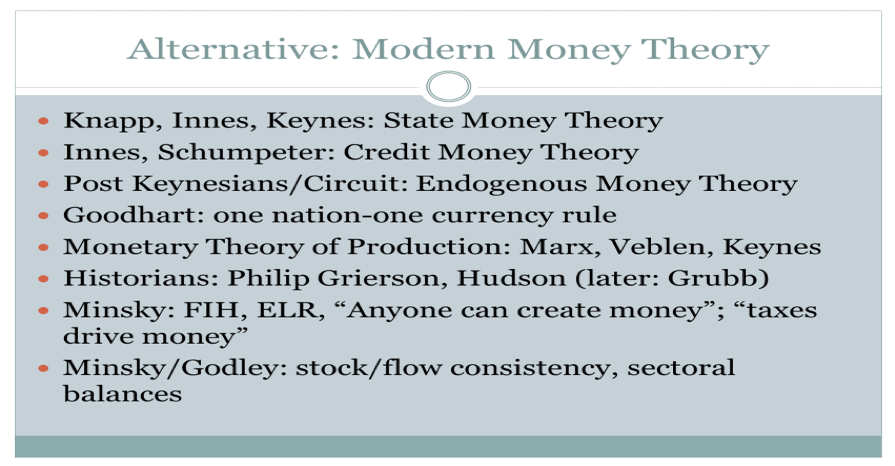

I objected to this characterization, showing my powerpoint slide from the year 2000 that laid out the various strands of thought incorporated in MMT up to that point. Here’s the slide I showed (with an update noted):

Notably missing was reference to functional finance. In fact, the core of MMT was developed before Lerner was brought into it (by Mat Forstater and Stephanie Kelton in the late 1990s). Most importantly, we ALREADY had our full employment policy: the Job Guarantee (also called employer of last resort, public service employment and buffer stock employment). It was from the very beginning THE central stabilizing component of MMT. Many of our neoliberal critics (who HATE full employment) have always tried to separate the JG from MMT. Josh follows in that tradition. We have always insisted that the JG is inseparable from MMT.

What do you get if you take the JG out? Josh’s neoliberal interpretation of MMT. MMT DOES NOT rely on aggregate demand pump priming to get to full employment. Never has. Never will. That will not work.

In 2005 Bill Mitchell and I argued that if desired, JG can be implemented to achieve full employment WHILE REDUCING AGGREGATE DEMAND.[2] To be sure, we’d recommend that only in very special circumstances, where the economy was already operating beyond full capacity—ie in a major war like WWII. Why would you need the JG if you were beyond full capacity? Because even when aggregate demand is very high, some get left behind. We do not think anyone should be left behind—if anyone wants to work at the program wage, he/she should receive a job offer. Only a JG can ensure this human right—the right to work.

Let me be clear. In the neoliberal era we chronically operate below full employment. That is very obvious in Euroland, which is probably operating 25% or more below full capacity. Even the US today has substantial excess capacity—maybe on the order of 10%, maybe more (maybe less). We won’t know until we ramp it up. Further, operating close to full capacity will bring forth investment and more capacity. I have little doubt that we could achieve Chinese growth rates if we put our minds to it—and sustain them for at least several years.

However, we will need well-targeted spending to do that without sparking inflation. It is hard to imagine how you’d do a general pump-priming; and you really wouldn’t want that even if you could. There are no doubt many sectors of our economy that really are at full capacity. Others lag far behind with substantial excess capacity. The problem with the kind of pump-priming we took in the past (mostly through “military Keynesianism”) is that the spending was targeted to the most advanced sectors, with high unionization and oligopoly or monopoly pricing. Wages and prices there rose and boosted measured inflation rates. That is precisely what we want to avoid.

As I said it is hard to think of a general pump-priming; except perhaps sending a $5000 check to every resident. But even this wouldn’t affect all sectors equally. Most Americans, suffering under huge debt loads, would probably pay down some debt. The comfortably well-off would splurge on fancy restaurants and expensive spas that already have long waiting lists. Or add a gold-plated toilet bowl to their third yacht.

I’ve long argued that rising tides raise all yachts—not the little dinghies. here and here As Pavlina Tcherneva’s empirical work has proven here , that turns out to be true. More than all the gains from growth now go to the tippy top of the income distribution. No wonder the Neoliberals hate the JG approach and love the pump-priming approach. As Tom Palley complains, the JG would give income directly to the poor and they’d want food. Neoliberals love unemployment—it keeps the “help” hungry and cheap. They are our inflation-fighting force to keep the comfortable classes comfortable.

To sum up my response to Noah Smith. Yes, MMT does have another tool to maintain price stability. It is the JG approach to full employment. It has always been a core element of MMT. We have never relied the simplistic version of Functional Finance that was presented by Mason. It would take about five minutes of actual research to demonstrate this.

We do often refer favorably to several arguments of Lerner. His “money is a creature of the state” provided a clear summary of Knapp’s approach (actually best explained in the 1913 and 1914 articles by A. Mitchell Innes); this was always in MMT even from before the beginning as I had read Knapp in 1986 and put him in my 1990 book). Indeed we view that as the other side of the coin to the JG.

What we really like was Lerner’s application of Functional Finance to the budgeting process. The budget should be functional, not sound. That is, to achieve a functional purpose rather than to balance taxes and spending. I never liked the steering wheel metaphor see here —although it can be useful in arguing that it is crazy policy to just let the “market” economy swing from speculative excess to deep depression. But economies are far too complex to “steer” like a car. We can attenuate the swings, but capitalist economies will still swing. That’s the Minsky in MMT. Stability is destabilizing. Our job is never done.

Let me be fair to Josh. When I presented my argument on the panel at EEA, Josh Mason graciously accepted it and said he’d look into the MMT position more deeply. It won’t take much digging.

Turning to Brad’s challenge, some of the answers will now be obvious. Do we accept the elements he lists as fundamental to MMT?

Knapp: yes indeed. He’s always been there. But as noted above, I’d refer readers to Innes instead—simpler, and he much more clearly links State Money to Credit Money. (That shapes our response to another set of critics—who disingenuously claim we ignore private monies. I’d wager there are very few economists who have written more about the private financial system than me—except my colleague Bill Black–but I’m not pursuing that here.)

Lerner: dealt with above. What we reject is the aggregate demand approach to full employment and price (and financial) stability. As Minsky argued in the 1960s, pump-priming might get you to full employment but it will never produce sustainable full employment because it will generate financial and price instability. You have to use the JG. He was right then, and he’s right now. To be sure, the inflation constraint is far less binding now than it was in the late 1960s. Further, once we have the JG in place, its stabilizing features will allow us to operate with higher aggregate demand without fueling inflation. The base wage plus the pool of labor ready for hire out of the JG will stabilize wages and prices at higher aggregate demand; and the access to decent wages will reduce necessitous borrowing thereby reducing financial instability.

Minsky. Yep, he was there from the beginning. In fact he was there before the beginning—I studied with him in the early 1980s and that is where I first came across the JG (he called it ELR) and the concept that taxes-drive-money. And then there’s our approach to financial instability. He’s indispensable.

Vertical IS. Now that is a leap. The ISLM framework is completely incoherent. It is not stock-flow consistent. Even its creator—John Hicks—said he could no longer make any sense of it. I think Paul Krugman and Tom Palley are the only economists who still use it. I doubt Brad uses it, at least, hope not. I have never used it. I reject all mainstream models (an exasperated Wynne Godley came into my office a couple of decades ago and announced that every one he had looked at was incoherent). But I think all Brad means is that MMT rejects the notion that by changing interest rates the central bank can move the economy to full employment by stimulating interest-sensitive spending. And if that is what he means, I whole-heartedly agree.

Unlike Krugman, MMT argues this impotence is not restricted to the “lower bound” of zero interest rates. What MMT has always argued is that when the Fed lowers its rate target, we cannot say for sure whether the Fed is stepping on the gas or hitting the brakes. It depends. One factor that matters a lot is what is the ratio of government debt to nongovernment debt. If you are Japan (high government debt, low household debt), lowering rates almost certainly slows the economy (by sucking interest income out). I did a paper with my UMKC colleague Linwood Tauheed that showed that with low private debt, plausible spending propensities, and government debt above 60% of GDP it is possible that raising rates would stimulate the economy.[3]

Now, that does NOT describe today’s US economy—where nongovernment debt is something like 400% of GDP. I believe that “normal” changes of the Fed’s target rate (up or down) have very little impact on the US economy. However a huge Volcker-like hike does have a big effect—but not due to interest-sensitivity of spending. It works through a present value reversal: the returns to holding real assets go negative. No one will invest in new ones. Debtors with floating rates go bankrupt. Financial institutions go massively insolvent. Volcker monetary policy “works” by causing a debt crisis. Otherwise, raising rates gradually in a boom (like the Fed did after 2004) doesn’t work; it does not reduce the demand and supply of loans, it just puts the debtors in a more precarious situation and shifts more income to the creditors. It is a dangerous policy. And no central bank official would admit they’d even consider such a policy. They prefer the myth that small adjustments to rates affect spending decisions. A myth with no evidence behind it, but so widespread that no one seeks evidence.

So, MMT has always recommended abandoning any attempt to fine-tune the economy through central bank interest rate policy. We prefer a permanently fixed rate. Many MMTers prefer permanent ZIRP. I’m a bit of a fence-sitter. I’d like ZIRP but I’d also accept a policy of paying a higher rate on retirement savings—but that is easily handled through US savings bonds, with personal limits on accumulations receiving the favorable rates. This rate should not be discretionary and should not be used as an inflation-fighting tool, rather as a supplement to Social Security until we can reform that system to provide a decent retirement for all. For me it is the permanent fixing that really matters, and I like a low rate but do not insist on zero.

So there you go, Brad, the ball’s in your court. We seem to be on the same page.

And by the way, I like Brad’s recent call for all the neoliberal Democrats to step aside and let the progressives following MMT take over. See Bill Black’s analysis here

[1] Blanchard announced he’s writing a piece(here ); McCulley’s supportive article is here, and he argues MMT provides a “robust architecture for a fiat currency world”; Fink called MMT “garbage”.

[2] Mitchell, W.F. and Wray, L. R. 2005 “In defense of employer of last resort: a response to Malcolm Sawyer” Journal of Economic Issues.

[3] Wray, L.R. and Linwood Tauheed) Chapter 3: “System dynamics of interest rate effects on aggregate demand”, pp. 37 in edited volume (Wray with Mathew Forstater), Money, Financial Instability and Stabilization Policy, Edward Elgar Publishing, 2006.

11 responses to “MMT Responds to Brad DeLong’s Challenge”