Twitter allows one to spread certain concise statements exceptionally quickly, but it is a vain effort to hold a serious and nuanced discussion via Twitter. I offer my twitter exchanges with two of Deal Book’s financial reporters on the subject of the New York Times story discussing the Manhattan DA’s indictment of the former leaders of the failed Wall Street law firm Dewey & LeBoeuf as an example.

The indictment alleges facts that if true would demonstrate that they were running the firm as an accounting control fraud for several years before it collapsed.

The articles

I have just posted an article criticizing Deal Book’s article. My article focuses on the ethical and legal implications of Deal Book’s claims about corporate counsel contained in the first sentence (the “lede”) of their article.

“Several former leaders of the once-high-flying law firm Dewey & LeBoeuf apparently violated a cardinal rule that lawyers always tell their clients: ‘Don’t put anything incriminating into an email.’”

(I have added the internal quotes for clarity. These are the words that corporate lawyers purportedly “always tell their clients.”)

My first article explains why such a “cardinal rule” of advising corporate officers (who are not our clients – but are the people who decide whether we are hired, fired, and paid) how to loot our corporate client with impunity by preventing the creation of a trail of “incriminating” evidence would be unethical and likely criminal. (“Incriminating” means that the evidence can establish the existence of a crime.) As lawyers, we cannot aid the commission of a felony. I then explain the profound and devastating consequences that would make finance endemically fraudulent were corporate lawyers to have such a “cardinal rule.”

I explain that corporate lawyers have no such “cardinal rule,” but that corporate CEOs running control frauds do select that small percentage of lawyers willing to aid such frauds. I then emphasize Deal Book’s continuing refusal to deal seriously with ethics or even endemic financial control fraud. Its column ignores the implications of the alleged fraud by Dewey’s controlling partners and focuses instead on the purported irony of those partners being indicted because they ignored their own “cardinal rule” against leaving an electronic trail of “incriminating” evidence.

The tweets

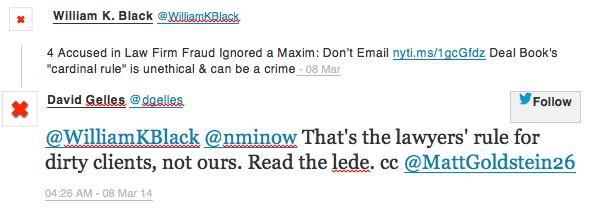

When I read the Deal Book article on Dewey I tweeted a message and received a response from what I initially assumed (incorrectly) must be the lead author of the Deal Book article on the indictment of Dewey’s former controlling partners.

When one uses twitter to reference and comment on an article the number of characters one can use in the message is ridiculously low. My available message length was about 60 characters. In fairness, the same constraint applies to the Deal Book reporters who replied to my tweets so I am writing this article in part to induce them to explain what they thought they were claiming about the purported rule.

Gelles’ tweet is deeply disturbing on many levels. I promptly made several of these points in a series of Twitter replies to him to which he did not respond. Yes, we all understand that Deal Book attributes the purported “cardinal rule” to corporate lawyers and that Deal Book is not praising lawyers’ (purported) “cardinal rule.” Deal Book claims that lawyers “always” advise corporate “clients” how to avoid leaving a trail of “incriminating” evidence that the government can use to prosecute the clients’ crimes. As I explained to Gelles; the purported cardinal rule would require lawyers to act unethically and even criminally.

In my prior article I explained the extraordinarily harmful logical implications for our world if Deal Book were correct in ascribing such a cardinal rule to my first profession and I explained that Deal Book ignores those implications. While Deal Book does not praise the (purported) “cardinal rule” it also gives no indication that it is condemns the rule and views it as certain to cause immense damage to finance, the economy, ethics, equality, and our democracy. Instead, Deal Book wants its readers to know how ironic it is that Dewey’s partners have been indicted because they failed to follow the advice they “always” give clients not to leave a trail of “incriminating” evidence documenting their frauds. When corporate officers engage in fraud it is common for them to defraud their firm. As I explain in my article about Deal Book’s coverage of the indictment of Dewey, Deal Book thinks lawyers “always” advise corporate officers how to commit crimes with impunity even when the unfaithful officer is using that advice to defraud the lawyer’s client – the corporation – in a manner most likely to escape detection by the internal and external auditors, the regulators, and the prosecutors. Deal Book’s journalists deal frequently with Wall Street lawyers, so it is startling that Deal Book believes in the universal depravity of corporate lawyers. That universal depravity could only exist if corporate officers wanted to hire unethical lawyers willing to aid and abet the officers even when they looted the lawyer’s clients. It is also startling (and depressing) that Deal Book cannot call forth enough courage to condemn what it presents as the universal depravity of Wall Street lawyers and the officers controlling their corporate clients. Deal Book specializes in a degree of sycophancy so extreme that even when Deal Book makes factual claims that logically require the universal depravity of Wall Street this isn’t sufficient to cause them to take crime and ethics seriously. Instead, they pitch the Dewey story as ironic tale of humor.

I read Gelles’ tweet as clarifying Deal Book’s belief that advising corporate clients’ officers about how to commit crimes – including defrauding the client – with impunity was only the “cardinal rule” of lawyers advising “dirty clients.” I agree, but Deal Book has plainly not thought through the logical implications of that fact. It would be obscene for a lawyer to “always” advise corporate officers how to commit fraud without creating an “incriminating” trail that could lead to the discovery and prosecution of the officer. Corporate lawyers know that a corporate officer’s most tempting fraud target is the officer’s own corporation, so advising officers how to defraud with impunity is depraved conduct for a lawyer.

Gelles fails to understand the still staggering implications of his statement that what Deal Book really meant to say in its article was that the lawyers’ “cardinal rule” is actually not to “always” advise corporate officers how to defraud with impunity by minimizing the creation of “incriminating” evidence. Instead, Deal Book meant to state that the lawyers’ “cardinal rule” of advising corporate officers how to defraud with impunity only applies when the lawyers are representing “dirty clients.” One hopes that “dirty clients” (a typical Deal Book euphemism for control frauds) represent a small subset of corporations. That is quite a retreat from what Deal Book wrote in its article. The article claims that lawyers “always” advise corporate officers of the purported “cardinal rule.”

Even after this major retreat from the “cardinal rule” that Deal Book presented as a fact in its article, Deal Book has announced a rule of terrible import (and ignored the import). Deal Book concedes that the fraudulent CEOs are easily able to select elite attorneys who are willing to aid and abet the CEOs’ looting of the firm through accounting control fraud. Unless one believes that elite Wall Street attorneys have particularly weak ethical standards, this should lead Deal Book to consider whether a CEO leading an accounting control frauds is similarly able to select readily for auditors, appraisers, and credit rating agency leaders willing to aid the CEO’s looting of the firm. Indeed, in the context of general corporate representation (as opposed to a being retained to defend and officer indicted for fraud), the obvious questions (except to Deal Book) are:

- Why do elite Wall Street law firms eagerly compete for the representation of corporations whose leaders they know to be “dirty” (fraudulent) and continue that general corporate representation when they know that their work is aiding the controlling officers looting of the client?

- Why do elite Wall Street law firms follow Deal Book’s (greatly revised) “cardinal rule” of advising the controlling officers they know to be “dirty” because they are looting the client how to do so without leaving a trail of “incriminating” evidence of the officers’ crimes that the auditors or regulators might spot and use to put an end to the looting and prosecutors could use to prosecute the fraudulent officers?

- If elite lawyers “only” employ their corrupt “cardinal rule” of giving unethical and even criminal when the corporate clients they are supposedly representing (but actually betraying) are controlled by “dirty” (fraudulent) officers, then isn’t it critical that Deal Book learn all it can about control fraud and educate its readers about this vital concept?

- Why doesn’t Deal Book warn about these control frauds, seek to identify them, and urge policy changes to end the criminogenic environments that can produce epidemics of control fraud?

- Why doesn’t Deal Book emphasize the critical managerial and professional ethics issues that run throughout these perverse dynamics?

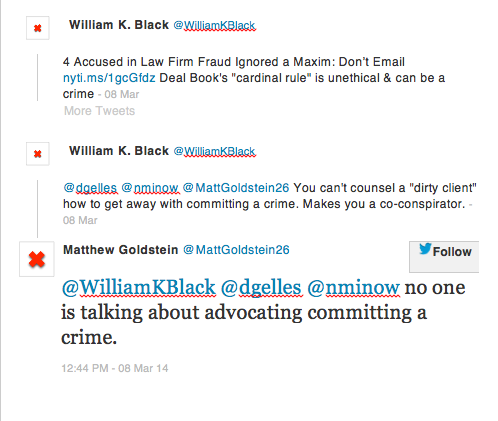

As I noted above, I need to, and do, apologize for the error of identifying in my prior article Gelles as the principal author of the Deal Book article on Dewey. Matthew Goldstein is the principal author. Goldstein replied (on Twitter) to one of my Twitter replies to Gelles’ reply to my initial post. Here is the chain.

I repeat the same caution about the limits of Twitter in expressing complex views and I encourage Goldstein to set out his views explicitly in an article if he feels that his tweet did not accurately reflect his true views. It is correct that none of us “advocate[e] committing a crime” in our tweets or articles. The “cardinal rule,” (either the one stated in the Deal Book article or the version stated in the radical retreat contained in Gelles’ tweet), does encourage crime by corporate officers. Indeed, that is the sole purpose of the unethical and even criminal legal advice contained in the Goldstein and Gelles versions of the purported “cardinal rule.” The sole reason that Deal Book presents for that legal advice is to aid the corporate officers to commit a crime with a greatly reduced risk of being sanctioned or prosecuted. The means of reducing the risk of sanction and prosecution are not by giving legal advice and counseling the officers to act legally and ethically and to honor at all times their fiduciary duties of care and loyalty. The sole means presented by Deal Book is to commit the crime while minimizing the “incriminating” evidence of the crime left as a potential trail. Giving such advice has to greatly increase the commission of crimes by the officers. Many of those crimes will be committed against the client. The legal profession’s (purported) “cardinal rule,” as described by Goldstein’s article and Gelles’ tweet do “[encourage] committing a crime.” The logical implication of their versions of the purported “cardinal rules” logically mean that lawyers advising corporate clients’ officers “always” (Goldstein’s version) give legal advice that encourages fraud by those officers or “always” give legal advice that encourages fraud by the officers when the controlling officers are “dirty” (fraudulent) (Gelles’ version) .

Goldstein’s use of “advocating” is a red herring. If lawyers “advocate[ed] committing a crime” they would be acting directly contrary to the theory of avoiding the creation of “incriminating” evidence. “Advocating committing a crime” to a group of corporate officers creates exceptionally incriminating evidence against both the lawyers and the corporate officers who follow the lawyers’ advice. A corporate officer who is prosecuted cannot argue as a defense that he lacks the required mens rea because he relied on the legal advice that consisted of saying (a) committing the following acts is a crime and (b) I encourage you to commit a crime. The relevant issue is whether Deal Book’s rival versions of lawyers’ purported “cardinal rule” would encourage officers to commit crimes by explaining to them how they can commit crimes without leaving the “incriminating” evidence trail. The answer to that question is: “yes.”

And a late entry by Deal Book’s (“I like to watch”) Peter Henning

Peter Henning has written a March 10, 2014 column (entitled “The Challenge of Linking Dewey’s Leader to Possible Accounting Shenanigans”) for Deal Book that recasts the “cardinal rule” as a very different “maxim.”

“As DealBook pointed out, the leaders at the firm seemed to have ignored the maxim to never put anything about questionable conduct in writing.”

The column is Henning’s effort to emphasize the difficulties of prosecuting even blatant acts of accounting and securities fraud like Dewey’s. There are three things in Henning’s column that are relevant to the topics I am discussing. First, as a law professor he isn’t about to make the mistake of claiming that lawyers have the “cardinal rule” that Deal Book ascribed to them. Second, Henning, who has literally written a book on securities fraud, uses one of the more obnoxious euphemisms for fraud – “shenanigans.” The word choice is designed to minimize the importance and culpability of elite frauds. It is a typical Deal Book ploy, but it is sad to see a professor who teaches white-collar crime employ such a classic and harmful “neutralization” device. Third, I finally noticed one of the best indicators of Deal Book’s pathology that has been staring me in the face for years. If you had asked me what the name of Henning’s Deal Book column was I would have answered “White Collar Crime Watch.” But that was another error on my part. Henning, a law professor who writes primarily about white-collar crime has a “branded” column on Deal Book that is actually entitled “White Collar Watch.”

When Deal Book was being “re-launched” its flack gave special praise to Henning’s column – which he described as “White Collar Crime Watch.”

Deal Book has so bowdlerized the reporting of Wall Street’s (and the City of London’s) epic white-collar crime sprees that drove our three modern financial crises that it has overwhelmingly removed the word – and the concept – of Wall Street “crime” from its columns. Henning, who has long been a defender of corporate elites, does not even brand his columns as covering white-collar crime. He “watches” (from Detroit) people who work on Wall Street and wear a “white collar.” If you think about it even a little the bowdlerized title of his column: “White Collar Watch” is ready-made for a Jon Stewart skit. It brings to mind the mindless mantra of Peter Seller’s character in the 1979 movie hit (Being There) of the gardener mistaken by the media for a sage: “I like to watch.”

Henning writes apologias for Wall Street elites in the rare cases where there frauds are prosecuted. Here’s the really bad news – his apologias are the toughest things Deal Book writes. In the Valley of the Blind, the apologist passes for the sentinel.

Pingback: Bill Black Slams New York Times for Wink and Nod Endorsement of Criminal Conduct | naked capitalism