(via Huffington Post)

The new mantra of the Republican Party is the old mantra — regulation is a “job killer.” It is certainly possible to have regulations kill jobs, and when I was a financial regulator I was a leader in cutting away many dumb requirements. But we have just experienced the epic ability of the anti-regulators to kill well over ten million jobs. Why then is there not a single word from the new House leadership about investigations to determine how the anti-regulators did their damage? Why is there no plan to investigate the fields in which inadequate regulation most endangers jobs? While we’re at it, why not investigate the areas in which inadequate regulation allows firms to maim and kill. This column addresses only financial regulation.

Deregulation, desupervision, and de facto decriminalization (the three “des”) created the criminogenic environment that drove the modern U.S. financial crises. The three “des” were essential to create the epidemics of accounting control fraud that hyper-inflated the bubble that triggered the Great Recession. “Job killing” is a combination of two factors — increased job losses and decreased job creation. I’ll focus solely on private sector jobs — but the recession has also been devastating in terms of the loss of state and local governmental jobs.

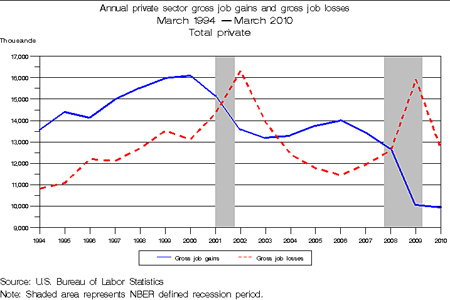

From 1996-2000, for example, annual private sector gross job increases rose from roughly 14 million to 16 million while annual private sector gross job losses increased from 12 to 13 million. The annual net job increases in those years, therefore, rose from two million to three million. Over that five year period, the net increase in private sector jobs was over 10 million. One common rule of thumb is that the economy needs to produce an annual net increase of about 1.5 million jobs to employ new entrants to our workforce, so the growth rate in this era was large enough to make the unemployment and poverty rates fall significantly.

The Great Recession (which officially began in the third quarter of 2007) shows why the anti-regulators are the premier job killers in America. Annual private sector gross job losses rose from roughly 12.5 to a peak of 16 million and gross private sector job gains fell from approximately 13 to 10 million. As late as March 2010, after the official end of the Great Recession, the annualized net job loss in the private sector was approximately three million (that job loss has now turned around, but the increases are far too small).

Again, we need net gains of roughly 1.5 million jobs to accommodate new workers, so the total net job losses plus the loss of essential job growth was well over 10 million during the Great Recession. These numbers, again, do not include the large job losses of state and local government workers, the dramatic rise in underemployment, the sharp rise in far longer-term unemployment, and the salary/wage (and job satisfaction) losses that many workers had to take to find a new, typically inferior, job after they lost their job. It also ignores the rise in poverty, particularly the scandalous increase in children living in poverty.

The Great Recession was triggered by the collapse of the real estate bubble epidemic of mortgage fraud by lenders that hyper-inflated that bubble. That epidemic could not have happened without the appointment of anti-regulators to key leadership positions. The epidemic of mortgage fraud was centered on loans that the lending industry (behind closed doors) referred to as “liar’s” loans — so any regulatory leader who was not an anti-regulatory ideologue would (as we did in the early 1990s during the first wave of liar’s loans in California) have ordered banks not to make these pervasively fraudulent loans.

One of the problems was the existence of a “regulatory black hole” — most of the nonprime loans were made by lenders not regulated by the federal government. That black hole, however, conceals two broader federal anti-regulatory problems. The federal regulators actively made the black hole more severe by preempting state efforts to protect the public from predatory and fraudulent loans. Greenspan and Bernanke are particularly culpable. In addition to joining the jihad state regulation, the Fed had unique federal regulatory authority under HOEPA (enacted in 1994) to fill the black hole and regulate any housing lender (authority that Bernanke finally used, after liar’s loans had ended, in response to Congressional criticism). The Fed also had direct evidence of the frauds and abuses in nonprime lending because Congress mandated that the Fed hold hearings on predatory lending.

The S&L debacle, the Enron era frauds, and the current crisis were all driven by accounting control fraud. The three “des” are critical factors in creating the criminogenic environments that drive these epidemics of accounting control fraud. The regulators are the “cops on the beat” when it comes to stopping accounting control fraud. If they are made ineffective by the three “des” then cheaters gain a competitive advantage over honest firms. This makes markets perverse and causes recurrent crises.

From roughly 1999 to the present, three administrations have displayed hostility to vigorous regulation and have appointed regulatory leaders largely on the basis of their opposition to vigorous regulation. When these administrations occasionally blundered and appointed, or inherited, regulatory leaders that believed in regulating the administration attacked the regulators. In the financial regulatory sphere, recent examples include Arthur Levitt and William Donaldson (SEC), Brooksley Born (CFTC), and Sheila Bair (FDIC).

Similarly, the bankers used Congress to extort the Financial Accounting Standards Board (FASB) into trashing the accounting rules so that the banks no longer had to recognize their losses. The twin purposes of that bit of successful thuggery were to evade the mandate of the Prompt Corrective Action (PCA) law and to allow banks to pretend that they were solvent and profitable so that they could continue to pay enormous bonuses to their senior officials based on the fictional “income” and “net worth” produced by the scam accounting. (Not recognizing one’s losses increases dollar-for-dollar reported, but fictional, net worth and gross income.)

When members of Congress (mostly Democrats) sought to intimidate us into not taking enforcement actions against the fraudulent S&Ls we blew the whistle. Congress investigated Speaker Wright and the “Keating Five” in response. I testified in both investigations. Why is the new House leadership announcing its intent to give a free pass to the accounting control frauds, their political patrons, and the anti-regulators that created the criminogenic environment that hyper-inflated the financial bubble that triggered the Great Recession and caused such a loss of integrity?

The anti-regulators subverted the rule of law and allowed elite frauds to loot with impunity. Why isn’t the new House leadership investigating that disgrace as one of their top priorities? Why is the new House leadership so eager to repeat the job killing mistakes of taking the regulatory cops off their beat?